“First they ignore you, then they ridicule you, then they fight you, and then you win.” Mahatma Gandhi

Bloomberg Releases an Unqualified Smear – A Good Sign?

We have previously remarked on the extremely poor quality of Bloomberg’s editing, mainly in the context of the site’s ongoing rape of the English language in its headlines. However, the quality of its editing processes has reached a new low when an unqualified and in places truly vile smear of the Austrian School of Economics recently slipped past its editors. Initially we didn’t plan to comment on it, simply because, as the Daily Bell has put it, “one doesn’t even know where to begin”. However, so many people have in the meantime mailed us the piece or a link to it that we feel compelled to address the article in a blog post.

We have previously remarked on the extremely poor quality of Bloomberg’s editing, mainly in the context of the site’s ongoing rape of the English language in its headlines. However, the quality of its editing processes has reached a new low when an unqualified and in places truly vile smear of the Austrian School of Economics recently slipped past its editors. Initially we didn’t plan to comment on it, simply because, as the Daily Bell has put it, “one doesn’t even know where to begin”. However, so many people have in the meantime mailed us the piece or a link to it that we feel compelled to address the article in a blog post.

The contributions of the Austrian School to the science of economics are as numerous as they are profound. Carl Menger contributed the theory of marginal utility (Jevons and Walras developed the same idea independently around the same time, so Menger wasn’t the sole originator), and a body of theory on value and prices that corrected many of the most glaring and profound errors of the classical economists. Incidentally, Menger also provided a sound explanation of the origin of money. Eugen von Böhm-Bawerk then followed in his footsteps with a highly advanced theory of interest and capital that inspired generations of successors.

In 1912, an at the time not yet widely known economist and pupil of Böhm-Bawerk by the name of Ludwig von Mises published “Die Theorie des Geldes und der Umlaufsmittel” (The Theory of Money and Credit), which established him overnight as Europe’s foremost monetary theorist. To this day Mises’ book must be regarded as the definitive work on money and credit, a work that has stood the test of time. Mises then published his seminal monograph “Economic Calculation in the Socialist Commonwealth”, which sparked the socialist calculation debate that raged with great intensity until the mid 1940s. Remarkably, the debate is still ongoing, in spite of the fact that Mises’ contentions were never refuted, and in spite of the fact that he has been proved right “in spades” by the economic disintegration of the Soviet command economies in the late 1980s. Two years later, Mises Published “Socialism – an Economic and Sociological Analysis”, which is one of the most profound and encompassing critiques of socialism ever written.

While working on his opus magnum “Nationalökonomie” (1938) – a treatise on economics that became better known in its revised English version as “Human Action” (1949), Mises published numerous articles in journals, many of which dealt with the systematization of the epistemological and methodological problems of economics. These remain a major bone of contention setting the Austrian school apart from other economic schools. Readers won’t be surprised that we are siding with the view that economics is not a science like physics and that the attempts to make it so have led the entire science astray.

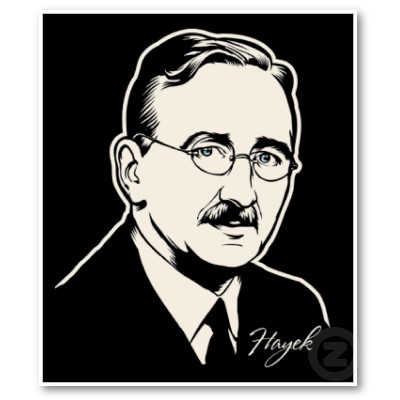

Friedrich A. Hayek, building on the works of Mises, provided outstanding contributions to capital and production theory (e.g. “Prices and Production”, “The Pure Theory of Capital” and numerous articles in economic journals), and later expanded the scope of Austrian theorizing with his writings on the nature of knowledge and entrepreneurship (see e.g. his famous essay “The Use of Knowledge in Society”). Hayek even received a Nobel Prize in Economics in 1974, in one of the few nods the establishment has given to Austrian economics (not that this really matters, we only mention it for the sake of completeness: Hayek’s Nobel lecture “The Pretense of Knowledge” in which he condemned the “scientism” of modern economics is certainly worth reading though).

Richard von Strigl, one of the few economists who didn’t flee Vienna (but certainly fell silent after the Nazi takeover) as a teacher not only greatly influenced Hayek, Machlup, Haberler, Morgenstern and many others, but left us with a unique contribution to capital theory with his work “Capital and Production” (1934).

We could continue this list up to the present, but in the interest of brevity, want to only mention Rothbard’s excellent sweeping economic treatise “Man, Economy and State” (1962; in Joseph Salerno’s words “a milestone in the development of sound economic theory, […] that rescued the science from self-destruction”) which presented a systematic and complete theory of production, as well as a unique and important revision of the theory of monopoly.

Well, scratch all that. These people were “infested by alien brain worms” according to the smear published at Bloomberg. The author, one Noah Smith, evidently knows nothing about Austrian economics – and we actually doubt that he really knows anything about other economic schools either. He has certainly never read or understood a single work by an Austrian economist. The whole thing simply reads like an ad hominem attack on supporters of the theory penned by a politically motivated hack. What is especially bizarre is his insinuation that Austrian economics somehow has “antisemitic overtones” – never mind, he says, that Ludwig von Mises and Murray Rothbard, two of the preeminent Austrian scholars were themselves Jews (not the only ones by the way), they’re antisemitic anyway!

We want to reprint the comment of Mr. Vincent Cook in this context (from the comments section at Bloomberg), who notes that an economic theory can hardly be refuted by mere name-calling, and addresses the above point in some detail:

“Mere name-calling doesn’t amount to a refutation of any economic theory, nor does the «guilt-by-association» tactic of linking certain adherents of a given economic theory to their empirical predictions not warranted by the theory itself or to their non-economic views on politics, etc. and claiming that such predictions and views somehow invalidate the theory.

If Mr. (Noah) Smith has any substantial objections to any element of Austrian economic theory that has been written over the past 140+ years, he should make the effort to cite the work in question and identify what specific premises or logical deductions he thinks the the Austrians got wrong. Characteristically Austrian ideas about the proper methodology of economics, about the nature of capital goods markets and interest rates, about the nature of boom/bust cycles, about the impossibility of economic calculation and coordination of decentralized information under central planning, etc. stand or fall on their own merits, not on what some fringe supporter of a political movement puts into a Youtube video.

The Austrian-oriented case for gold and for 100% reserve banking, for example, doesn’t depend on any belief about secret banker plots or about any mechanistic link between money creation and price increases. Rather, it is based on the desirability of preventing destructive boom/bust cycles, of eliminating any long-run risk of hyperinflation, of preventing money and money-substitute creation from becoming a source of political rent-seeking and moral hazard, and of upholding the integrity of the payments system without counterproductive regulatory interventions and bailouts. Mr. Smith’s misrepresentations of the case for gold and for 100% reserve banking are simply irrelevant to the issue at hand.

Mr. (Noah) Smith’s neo-Nazi baiting is particularly scurrilous, as it grossly misrepresents the attitudes that Austrian economists have always had about the Nazi movement. Ludwig von Mises wasn’t simply a Jewish Austrian economist (and one had to flee Vienna ahead of the Anschluss), he also wrote books concerning the ideological development and political growth of militant German nationalism that are still in wide circulation among contemporary Austrian economists and that still strongly inform their understanding of the subject. Indeed, Mises’s 1919 work Nation, State and Economy and his 1944 work Omnipotent Government are must-reads for anyone who wants to understand what went wrong in Germany.

I challenge Mr. Smith and anyone who takes Mr. Smith seriously to read these works and others concerning German history and the Nazis that circulate among Austrian economists (such as Günter Reimann’s The Vampire Economy). There is not the slightest trace of anti-Semitism in them, and anyone with any sense of honor and decency reviewing this literature will recognize that Mr. Smith owes the entire contemporary Austrian school an apology.”

We doubt that such an apology will be forthcoming, or that Mr. Smith will make the effort to actually read any Austrian economists. Obviously his article was never intended to be a serious critique – it is simply a hit piece. What is interesting about it is mainly that Bloomberg allowed it to be published. We have put Mahatma Gandhi’s famous quote at the beginning of this article for a reason. Before the advent of the internet, it was easy for the establishment to “bury” the Austrian School’s causal-realist approach to economics by simply ignoring it. Evidently, we have now progressed to somewhere between point 2 and 3 of Gandhi’s list – the ‘ridiculing and fighting’ stage. We can take this as a sign of progress. Ignoring the Austrians is no longer deemed sufficient.

Carl Menger, the founder of the Austrian School

Carl Menger, the founder of the Austrian School

(Photo via Wikimedia Commons)

A Few Remarks on Concepts Discussed by Smith

One of our readers who pointed the Bloomberg article out to us remarked that such attacks often occur close to economic and financial turning points. Readers may recall that practically the entire mainstream economic profession woke to a considerable amount of egg on its face after the 2008 crisis, as the vast majority of economists had neither predicted it, nor provided even the slightest warning of the growing imbalances in the economy that eventually led to the bust. One quite prominent economist who got it completely wrong was of course Ben Bernanke, the former Fed chairman. To state that he merely “didn’t see it coming” doesn’t fully describe the enormity of his forecasting errors (see this video). The public not unreasonably began to wonder what economists are actually good for.

In the two years prior to the crisis is was however highly fashionable to ridicule and attack supporters of the Austrian School, who were indeed among the very few economists who actually did predict the crisis – in spite of the fact that they do not regard “prediction” to be among the tasks of economic theory. Prediction is akin to the study of history, a thymological task. Correct economic theory and praxeological reasoning can be helpful with respect to forecasting, in that they help with delineating the constraints of such forecasts. But forecasting as such is basically the job of entrepreneurs and speculators, not that of economists.

An entrepreneur who evinces a sound understanding of Austrian theory is Peter Schiff, who was featured prominently in televised debates on financial markets and the economy as the “token bear” in 2005 to 2007, as a foil for all the other debaters who kept insisting that everything was fine until it could no longer be denied that catastrophe had struck. Again, to say that Schiff was “ridiculed and attacked” in his appearances in those years does not fully convey the viciousness and arrogance some of his opponents displayed (there are two videos on you-tube documenting this – one ‘general video‘ covering a range of appearances and the ‘CNBC edition‘).

This fits with our reader’s observation that such attacks tend to become especially pronounced near turning points. It took the establishment-approved defenders of the central planning statist quo a little while to get their courage up after the collapse of the tech bubble, and when they finally felt confident enough to declare that the printing press had triumphed, the next denouement wasn’t far away. In that sense, the Smith article can be seen as a hint that the current inflationary boom may also be close to meeting its inevitable fate.

Professional economic forecasting in a nutshell

Professional economic forecasting in a nutshell

This brings us to several points raised by Smith which deserve some additional comment. Smith inter alia mentions that Austrian economist Robert Murphy “lost a bet on inflation” with someone. However, economics is not about winning bets, and as noted above, it is not about making predictions either. This is in spite of the fact that the Econometric Society’s original motto was “Science is Prediction”. As Rothbard points out in Man, Economy and State:

“Praxeology and economics deal with any given ends and with the formal implications of the fact that men have ends and employ means to attain them”

In short, economics is the study of the purposive employment of (scarce) means to attain ends. The formal implications thereof form the basis of economic laws, which have universal, time- and place-invariant validity.

The debate over inflation is apparently Smith’s biggest bug-bear, as he devotes large parts of his screed to the topic. This is perhaps no surprise, as his main concern appears to be the defense of central banking, or putting it in more general terms, the defense of central economic planning by organs of the State.

In the process, he gets all sorts of things wrong. For instance, he alleges that the absence of a sharp rise in consumer prices to date in spite of the Federal Reserve’s relentless money printing caused Austrians to “redefine inflation”. Here is the relevant passage from his article:

“The Austrians’ next defense was to redefine reality. Inflation doesn’t mean a rise in prices, they said – it means an increase in the monetary base. QE wasn’t causing inflation, it was inflation itself. Duh! Now the Austrians were safe — after all, you can define inflation as anything you want. It’s a free country, ain’t it? You can define inflation to be a rare poisonous South American tree frog if you want, and the only consequence will be that people think you’re off your rocker. And so when Austrians tried to redefine the word “inflation” to mean something other than “a rise in prices,” people duly recognized that Austrians were off their rockers.”

We haven’t heard from all those people who allegedly “duly recognized that Austrian’s were off their rockers”, so we are guessing that by “people”, Smith mainly refers to himself. First of all, it should be pointed out that there is a formal mistake in this paragraph, as no Austrian has ever asserted that “increases in the monetary base” constitute inflation. The monetary base consists of two major components, only one of which, namely currency, is part of the money supply. The far greater part of the monetary base nowadays consists of bank reserves, which are explicitly excluded from definitions of the money supply. While they provide the basis for the inflationary pyramiding of credit, they are themselves not “money” (although they can become part of the money supply when they are transformed into currency upon customer withdrawals from demand deposits).

More importantly though, Austrians did not suddenly “redefine the meaning of inflation”. The redefining was done by others, as inflation had always denoted an increase in the supply of money, before its meaning was deliberately changed to mask the chain of cause and effect. In his essay “Inflation and Price Control”, published in 1945, Ludwig von Mises remarked that this redefinition of the term inflation was by no means harmless:

Inflation must result in a general tendency towards rising prices. Those into whose pockets the additional quantity of currency flows are in a position to expand their demand for vendable goods and services. An additional demand must, other things being equal, raise prices. No sophistry and no syllogisms can conjure away this inevitable consequence of inflation.

The semantic revolution which is one of the characteristic features of our day has obscured and confused this fact. The term inflation is used with a new connotation. What people today call inflation is not inflation, i.e., the increase in the quantity of money and money substitutes, but the general rise in commodity prices and wage rates which is the inevitable consequence of inflation. This semantic innovation is by no means harmless.

First of all there is no longer any term available to signify what inflation used to signify. It is impossible to fight an evil which you cannot name. Statesmen and politicians no longer have the opportunity to resort to a terminology accepted and understood by the public when they want to describe the financial policy they are opposed to. They must enter into a detailed analysis and description of this policy with full particulars and minute accounts whenever they want to refer to it, and they must repeat this bothersome procedure in every sentence in which they deal with this subject. As you cannot name the policy increasing the quantity of the circulating medium, it goes on luxuriantly.

The second mischief is that those engaged in futile and hopeless attempts to fight the inevitable consequences of inflation-the rise in prices-are masquerading their endeavors as a fight against inflation. While fighting the symptoms, they pretend to fight the root causes of the evil. And because they do not comprehend the causal relation-between the increase in money in circulation and credit expansion on the one hand and the rise in prices on the other, they practically make things worse.”

(emphasis added)

In addition, it should be mentioned than no Austrian economist has ever asserted that an increase in the supply of money must instantly and definitely lead to rising consumer prices (even if some have said they expected it to happen, there is nothing apodictic about it). In fact, as Mises pointed out in 1912 already, it is futile to even pretend that something like the “general level of prices” can be measured, as the exchange value of money depends on altogether four factors: the supply of money, the demand for money, and the supply of and demand for goods and services.

This is inter alia why the former correct usage of the term inflation is so important. The effects of vast increases in the money supply can be masked by a concomitant increase in productivity and the supply of goods. This is what happened e.g. in the boom of the 1920s – and it seriously misled many economists as well as the central bank at the time, as they were convinced that because consumer prices had not increased, nothing was amiss. As we know today, the boom eventually turned into the Great Depression, so this was a rather grave error in retrospect. One must surely agree with Mises that the semantic confusion regarding the term inflation is anything but harmless. However, to return to Smith, it wasn’t the Austrians who redefined the term inflation, and they most certainly didn’t do so recently because they are allegedly miffed that CPI has not yet risen much in the face of a 95% increase of the broad US money supply since 2008.

Ludwig von Mises. It just might be that he knew a little bit more about inflation than Noah Smith

Ludwig von Mises. It just might be that he knew a little bit more about inflation than Noah Smith

(Photo via Wikimedia Commons)

As an aside, Mises was inter alia concerned about the long term effect of monetary inflation on money’s general purchasing power, because he had experienced several destructive hyper-inflation episodes in his lifetime, and had seen firsthand what enormous economic, social, and political damage the breakdown of monetary systems can cause. However, as Mises and other Austrian economists have never tired to point out, monetary inflation causes a “price revolution” in that it most definitely alters relative prices in the economy, even if consumer prices fail to increase much. This is in fact the most pernicious effect of inflation, as it is the root cause of the boom-bust cycle, by dint of falsifying economic calculation.

Moreover, contrary to what Smith appears to think, Austrian economists are not particularly concerned about short term fluctuations in the gold price. They would undoubtedly regard a rising gold price as one of inflation’s possible effects, and a warning signal indicating that economic confidence is waning. The Austrian support for employing gold as money is also a bit more differentiated than Smith makes it out to be. The main point Austrians are making is that money should be left to the market. Whether market participants will choose gold or something else is not of central importance, although history certainly suggests that gold would play an important role in a free market money system.

Lastly, we want to briefly address the 5 points Smith lists at the beginning of his article as the ‘Austrian beliefs’ he intends to denigrate. These are:

“1) Federal Reserve money-printing is a government plot to boost big banks, 2) prices are rising much faster than anyone thinks, 3) real “inflation” means money-printing, not an increase in prices, 4) printing money can never boost the economy, 5) academic economics is a plot to use mathematical mumbo-jumbo to cover up government giveaways to big banks, etc., etc.”

We’re not sure what is meant by “ect., etc”, so we can only address the five points explicitly mentioned.

1. As to the first point, well, check, what else does Smith think Federal Reserve money printing since 2008 was about? Rescuing dairy farmers in Kansas?

2. As to point two, he doesn’t mention which prices, but as noted above, a ‘general price level’ can actually not be calculated, so while measures like CPI may serve as a rough approximation of consumer price trends, they certainly don’t tell the whole story. Since March of 2009, the prices of titles to capital have for instance increased by an average of 190%. This is one of the signs that the above mentioned distortion in relative prices is well underway.

3. We have addressed point three extensively above, as it seems to us it is an especially important one. Just one more remark that has to do both with the second and the third point: there is no way to predict with certainty whether and at what point an increase in the money supply will lead to large and broad-based losses in money’s purchasing power. This depends largely on contingent circumstances. For instance, if the monetary authority abandons the inflationary policy in time, i.e., before the public’s inflation expectations change, it may never happen. We may merely get a sizable economic bust instead. On the other hand, the progression from “lots of money printing” to “inflationary breakdown of the underlying currency system” could be observed several times in history, and what all these historical examples have in common is that there were large time lags between the money supply expansion and the point when the public came to realize that the inflationary policy wouldn’t be stopped and lost confidence in the currency. As Mises wrote on this:

“This first stage of the inflationary process may last for many years. While it lasts, the prices of many goods and services are not yet adjusted to the altered money relation. There are still people in the country who have not yet become aw-are of the fact that they are confronted with a price revolution which will finally result in a considerable rise of all prices, although the extent of this rise will not be the same in the various commodities and services. These people still believe that prices one day will drop. Waiting for this day, they restrict their purchases and concomitantly increase their cash holdings. As long as such ideas are still held by public opinion, it is not yet too late for the government to abandon its inflationary policy. But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against «real» goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against them.”

(emphasis added)

Note that we are not saying that this is what will necessarily happen this time. We merely wish to point out that firstly, it is bound to happen if the inflationary policy is not abandoned in time, and we secondly want to stress the point that there can be very large time lags before the effects of an expansion of the money supply become noticeable in the prices of consumer goods. In short, there is currently no proof whatsoever that these effects won’t appear.

Ben Bernanke’s ideas about monetary policy summarized

Ben Bernanke’s ideas about monetary policy summarized

(Cartoon by Lewis)

4. Point four is one we have discussed extensively in these pages on many previous occasions. Austrians have never said that money printing cannot “boost the economy”, since obviously, money printing is what causes economic booms. Hence, “economic activity” may well increase statistically when the central bank expands the money supply (note that this is not always the case). What we are saying is something entirely different: namely that money printing cannot possibly increase society’s wealth; rather, it tends to achieve the exact opposite. The supply of capital goods cannot be increased by printing money; if it could, Zimbabwe and Venezuela would be rich instead of being economic basket cases. Money printing leads to a false prosperity, as the boom is characterized by malinvestment and consumption of capital. A boom either collapses at some point, or – if the authorities continue to inflate – the entire underlying currency system will collapse as described above. These are the alternatives – there is no “good outcome”.

5. As to point five, quite a lot of economics nowadays indeed consists of mathematical mumbo-jumbo (mathematics should be banished from economic theorizing in our opinion; it cannot express anything that could not be better expressed verbally. It is merely an attempt to make economics look more “scientific”, but in reality it obfuscates rather than illuminates the topics discussed). As to the idea that many economists are statists, well, what can one say, except: guilty as charged! A free, unhampered market economy would have very little use for the great majority of today’s macro-economists. Many of them are directly or indirectly in the government’s employ and are paid wages far above their market value. It goes without saying that they will never bite the hand that feeds them.

Conclusion

In fact, with regard to the latter point, Austrians are inter alia clearly set apart from other economic schools in one crucial respect, and that is in their unstinting support of the free market. It matters little if this support is solely based on utilitarian reasoning or if it is also supported by ethical considerations. Clearly though, Austrians are saying that the market economy cannot possibly be improved by government intervention. Their views are also different from those of establishment-approved “free market supporters” such as Milton Friedman, whom Smith mentions approvingly. Friedman supported free markets, except in the context of central banking and money; for some reason, he considered the free market to be inferior in providing a sound monetary system. Given the absolutely central role interest rates and the money and credit supply play in the market economy, one may be excused for harboring doubts about Mr. Friedman’s free market credentials.

Austrian economists are therefore far less likely to find employ in state-supported institutions or to receive research grants from the central bank or similar agencies. One could say that they are actually diminishing their own career prospects in favor of standing up for the truth and their convictions. We can assure readers though that their failure to fall in line with the statism Smith evidently supports is not a sign of alien brain worm infection.

In fact, we are continually surprised by the eagerness with which people like Smith argue that freedom and support of freedom are somehow bad, and that being lorded over by the State is preferable. It is not as if Mr. Smith were a member of the ruling elite (at least we have never heard about him before), so one wonders what he gets out of his statolatry.

Murray Rothbard dispensing sound advice which Mr. Smith should take to heart.

Murray Rothbard dispensing sound advice which Mr. Smith should take to heart.

Source: Acting Man, 2014.

Existe, por supuesto, una “teoría económica de la política”, que se suele llamar “Teoría de la Elección Pública” o “Public Choice”. Ahora bien, ¿existe una teoría económica ‘austriaca’ de la política? Esto lo trata Michael Wohlgemuth en el interesante artículo titulado “La democracia como un proceso de descubrimiento: hacia una “economía austriaca” del proceso político” (Libertas 34, 2001).

Existe, por supuesto, una “teoría económica de la política”, que se suele llamar “Teoría de la Elección Pública” o “Public Choice”. Ahora bien, ¿existe una teoría económica ‘austriaca’ de la política? Esto lo trata Michael Wohlgemuth en el interesante artículo titulado “La democracia como un proceso de descubrimiento: hacia una “economía austriaca” del proceso político” (Libertas 34, 2001).