This week Eric Worre takes on Dave Ramsey… Recently during Dave’s radio show he had a woman call in regarding her opportunity in network marketing. Mr Ramsey’s response to this young lady’s questions were filled with misinformation about the profession and Eric Worre is here to set him straight on the truth about Network Marketing …

In the radio show, Dave asks this young lady, “Are you sure this is your dream? Are you sure that this is the best entrepreneurial way for you? You know, these network marketers, they make it sound so easy, but it’s hard. It’s hard work… And do you realize that for the rest of your life you’re just going to be recruiting? And is that really what you want to do? Do you want your friends looking at you funny because these network marketers drive everybody crazy? And what about getting stuck with product?” Dave went on to pour cold water all over the hopes and dreams of this young woman, and pigeon holed the Network Marketing profession into his very limited understanding of what it is all about.

This lit a fire under Eric, and he had this to say in rebuttal to Dave Ramsey, and also to the young woman (or any person) looking for an entrepreneur based business or looking for opportunity …

As far as entrepreneurial options, network marketing is the most financially responsible of all choices. The average person in the United States that wants to start a traditional business, spends $65,000 into a business that they know nothing about most of the time, and 90% of those fail over the course of five years. But in network marketing your investment startup is typically $1,000 or less. Also most companies have a 90% buy back policy, so the investment risk on $1000 is now down to $100. Network marketing is the most risk-free when it comes to just the dollars.

Another firing point was Dave told her that “all you’re gonna be doing is recruiting.” Eric offers this advice on how to actually explain it: “All you do is you expand your network and you expand the productivity of that network.” Which, as Eric points out, is exactly the same business model that Dave has followed… he expanded his radio network, he expanded his financial advisor network, and all of those advisors in every state, all over the world are providing advice for Dave within his network, and then giving him a little piece of the pie. The wealthy people in this world build networks, look for networks, and then increases the productivity of those networks. Network marketing is no different. It’s the same.

Eric also continues to provide rebuttal to the “it’s hard” comment, and the “bothering your friends” mentality that Dave and some people might have about the profession. There is a lot of misinformation about the network marketing profession floating around, and Eric sets the record straight on what is real and what to expect.

In conclusion, Eric has this to say — network marketing is not perfect, but it is better if you have an entrepreneurial bone in your body, it’s better. And to Dave Ramsey if he is listening, “You come into my world and talk about network marketing like you know it – I’ve got to call you on it. Sorry, man. And I respect your work, but in this case, you’re off base.” And for the young lady on the radio show, or anyone who is in the profession: “I hope someday we meet and you tell me your story about how you crushed it inside of this network marketing business and you took all the doubters, including Mr. Dave Ramsey, and you proved them wrong.”

These 13 annuity terms separate the novice from the expert.

Annuities have many benefits — security, flexibility, tax efficiency — but few would argue that simplicity is one of them. A successful sale is also an education process, uniquely tailored to the client. The foundation of all of this, of course, is the language. You may not have been directly asked about dollar cost averaging lately, but that doesn’t mean your clients don’t need to know what it is.

How well can you define some of the terms that are foundational to this product line? Keep reading to test your knowledge.

Variable annuity payments increase or decrease based on the net performance (returns after fees and expenses) of the underlying investments in relation to a benchmark assumed investment return. If the total investment return minus expenses exceeds the AIR, the payment increases. If the return minus expenses is less than the AIR, the payment decreases. If the return minus expenses equals the AIR, payments remain the same.

B-Share Variable Annuities

Variable annuity contracts characterized by deferred sales charges, which typically range from 5 percent to 7 percent in the first year, and subsequently decline to zero after five to seven years. B-shares are the most common form of annuity contracts sold.

Bonus Share (X-Share) Variable Annuities

A bonus amount, typically defined in the prospectus as a percentage of purchase payments, is allocated to the annuity accumulation value early in the contract period. This type of annuity typically has higher expenses to pay for the cost of the bonus.

Dollar Cost Averaging

A program for investing a fixed amount of money at set intervals with the goal of purchasing more shares at low values and fewer shares at high values. Variable annuity dollar cost averaging programs involve allocating a certain amount to one investment subaccount, such as a money market fund, and then having portions of that payment periodically transferred to other subaccounts. Dollar cost averaging does not guarantee a profit or prevent a loss in declining markets.

Exclusion Ratio

The formula that determines which portion of an annuity payment is considered taxable and which is a tax-free return of principal. For variable annuities, this formula is similar; however, due to the fluctuating nature of variable payouts, this is recalculated annually and is reported as an exclusion amount.

I-Share Variable Annuity

Also known as fee-based variable annuities in which an investor pays one fee to have the portfolio managed by an investment advisor. I-shares do not offer a sales commission to the advisor. However, the advisor assesses fees for the services, including the I-share contract, which is agreed upon by the client.

Immediate Annuity

An annuity purchased with a single premium on which income payments begin within one year of the contract date. With fixed immediate annuities, the payment is based on a specified interest rate. With variable immediate annuities, payments are based on the value of the underlying investments. Payments are made for the life of the annuitant(s), for a specified period, or both (e.g., 10 years certain and life).

Market Value Adjustment (MVA)

A feature included in some annuity contracts that imposes an adjustment or fee upon the surrender of a fixed annuity or the fixed account of a variable annuity. The adjustment is based on the relationship of market interest rates at the time of surrender and the interest rate guaranteed in the annuity.

O-Share Variable Annuities

Annuity contracts that do not impose up-front sales charges, while, typically, possessing surrender charge periods similar to B-shares. Mortality and expense charges are assessed, and progressively decline throughout the surrender period.

Private Annuity

A private annuity is an arrangement in which the client transfers property to an individual or entity in return for a promise of fixed periodic payments for the rest of the client’s life. In private annuities, the person or entity assuming the payment obligation is not in the business of selling annuities.

Systematic Withdrawal Plan

A distribution method that allows a variable annuity contract owner to periodically receive a specified amount as a partial withdrawal from the annuity contract value prior to the annuity starting date. Unlike lifetime annuity payments, systematic withdrawals continue until the contract value is exhausted. Systematic withdrawals are taxable to the extent they represent investment gain in the contract.

Unit Value

A measurement of the performance of the underlying funds in a variable annuity, similar to the share value of a stock. Each investment subaccount has a separate unit value. The unit value increases with positive investment performance in the subaccount and decreases with negative investment performance and with asset management and insurance charges.

Wrap-fee

A comprehensive charge levied by an investment manager or investment advisor to a client for providing a bundle of services, such as investment advice, investment research and brokerage services. Wrap fees allow an investment advisor to charge one straightforward fee to their clients, simplifying the process for both the advisor and the customer.

La crisis financiera dejó una bomba de tiempo por falta de liquidez

Por Nouriel Roubini.

NUEVA YORK – Desde la crisis financiera global de 2008 ha surgido una paradoja en los mercados financieros de las economías avanzadas. Políticas monetarias no convencionales han generado un exceso gigantesco de liquidez. Pero una serie de sacudidas recientes sugieren que la liquidez macro ahora está asociada a una severa iliquidez del mercado.

Las tasas de interés promovidas por las políticas están cercanas a cero y hasta debajo en la mayoría de las economías avanzadas, y la base monetaria (el dinero creado por los bancos centrales en efectivo y reservas líquidas de los bancos comerciales) ha aumentado -el doble, triple y cuádruple en los Estados Unidos- en relación con el período anterior. Esto mantuvo bajas las tasas de interés a corto y largo plazo (y negativas, como Europa y Japón), redujo la volatilidad de los mercados de bonos e hizo aumentar precios de activos.

Y, sin embargo, los inversores tienen motivos para preocuparse. Sus miedos comenzaron con el llamado «flash crash» de mayo de 2010, cuando, en 30 minutos, los principales índices bursátiles de Estados Unidos cayeron casi 10%, antes de recuperarse rápidamente. Luego llegó el «taper tantrum» en 2013: las tasas de interés a largo plazo de los Estados Unidos se dispararon 100 puntos básicos después de que el entonces presidente de la Reserva Federal, Ben Bernanke, sugirió su intención de poner fin a las compras mensuales de títulos a largo plazo por parte de la Fed.

De la misma manera, en octubre de 2014, los rendimientos del Tesoro norteamericano se derrumbaron casi 40 puntos básicos en cosa de minutos, algo que, a criterio de los estadísticos, debería ocurrir solamente una vez en 3000 millones de años. El último episodio se produjo apenas el mes pasado cuando, en espacio de pocos días, los rendimientos de los bonos alemanes a 10 años pasaron de cinco puntos básicos a casi 80. Estos episodios han alimentado los temores de que, incluso mercados muy profundos y líquidos -como las acciones estadounidenses y los bonos del gobierno en Estados Unidos y Alemania- tal vez no sean lo suficientemente líquidos. ¿Qué representa, entonces, la combinación de liquidez macro e iliquidez de mercado?

En los mercados de acciones, los operadores de alta frecuencia (HFT, por su sigla en inglés), que usan programas informáticos con algoritmos para seguir las tendencias de los mercados, son responsables de un porcentaje mayor de las transacciones. Esto crea un comportamiento de manada. De hecho, el trading hoy en los Estados Unidos se concentra en el comienzo y en la última hora de las operaciones diarias, cuando los HFT están más activos; el resto del día, los mercados son ilíquidos, con pocas transacciones.

Una segunda causa es que los activos de renta fija -bonos de gobierno, corporativos y de mercados emergentes- no se negocian en bolsas más líquidas, como las acciones, sino principalmente en mercados extrabursátiles ilíquidos.

Tercero, no sólo la renta fija es más ilíquida, sino que ahora la mayoría de estos instrumentos -que se han multiplicado debido a la emisión vertiginosa de deudas privadas y públicas antes y después de la crisis financiera- se mantienen en fondos abiertos que les permiten a los inversores salir a las 24 horas. Imaginen un banco que invierte en activos ilíquidos, pero permite a los depositantes hacerse de su efectivo en 24 horas: si se produce una corrida sobre estos fondos, la necesidad de vender activos ilíquidos puede llevar su precio a niveles muy bajos en poco tiempo, lo que consiste, en efecto, en una liquidación.

Cuarto, antes de la crisis de 2008, los bancos eran creadores de mercado en instrumentos de renta fija. Tenían grandes inventarios, ofreciendo así liquidez y aplacando la volatilidad excesiva de los precios. Pero con las nuevas regulaciones redujeron su actividad. Esta combinación de liquidez macro y de iliquidez de mercado es una bomba de tiempo. Es el resultado de las políticas para responder a la crisis financiera. La liquidez macro está alimentando períodos de bonanza y burbujas; pero la iliquidez de mercado terminará dando lugar a un descalabro y finalmente a un colapso.

—El autor es profesor de Economía en la Universidad de Nueva York.

Fuente: La Nación, 07/06/15.

——————————————

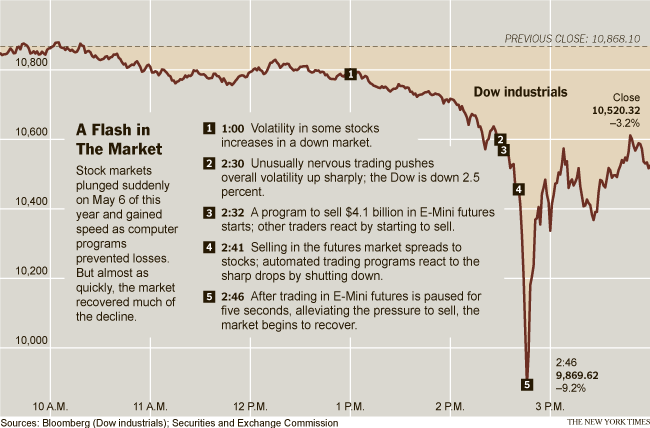

Flash Crash de 2010

El Flash Crash del 6 de mayo de 2010,1 también conocido como el Crash de 2:45, el Flash Crash de 2010 o simplemente el Flash Crash, fue una caída financiera estadounidense que tuvo lugar el 6 de mayo de 2010 en el que el índice Dow Jones Industrial Average se desplomó cerca de 1000 puntos, aproximadamente un 9%, para recuperar esa pérdida escasos minutos. Fue la segunda mayor caída en puntos, 1,010.14 puntos,2 y el mayor desplome diario, 998.5 puntos, en una base intradía en la historia del Promedio Industrial Dow Jones.345

Evento

El 6 de mayo de 2010, los mercados de valores de Estados Unidos abrieron con caídas y se mantuvieron bajistas durante la mayor parte de la jornada como consecuencia de la preocupación existente en el mercado por la crisis de deuda en Grecia. A las 14:42, cuando el índice Dow Jones acumulaba una caída de más de 300 en el día, el mercado de valores comenzó a caer rápidamente, bajando en más de 600 puntos en 5 minutos hasta alcanzar una pérdida de cerca de 1000 puntos en el día hacia las 14:47. Veinte minutos más tarde, hacia las 15:07, el mercado había recuperado la mayor parte de los 600 puntos de caída.6

Lauricella, Tom (7 de mayo de 2010). «Market Plunge Baffles Wall Street — Trading Glitch Suspected in ‘Mayhem’ as Dow Falls Nearly 1,000, Then Bounces». The Wall Street Journal. p. 1.

Book jacket of ‘Dark Pools’ by Scott Patterson. Random House

The chaotic listing of Facebook Inc. on the Nasdaq stock market last month was the latest example of how computer-trading systems can go haywire. The social network’s botched IPO came hard on the heels of another embarrassing glitch. In March, BATS Global Markets, a computer-driven exchange, failed to list its own stock due to a software bug.

Mishaps such as these are damaging the confidence of small investors in the integrity and reliability of stock markets, critics say.

The root of retail investors’ end of the love affair with the stock market can be traced back to May 6, 2010, the day of the now-infamous «flash crash.»

A dark pool is an electronic platform where investors trade shares privately, away from more transparent stock exchanges. What do they have to hide? Lam Thuy Vo shines a light on dark pools.

In the space of a few, hair-raising minutes, a breakdown in the market triggered by failures in computer-trading systems across the country caused stocks to plunge about 10%. Despite extensive probes by regulators, the cause of that sudden crash remains a mystery.

Advertisement

The flash crash left a scar on the market. Investors have taken money out of the U.S. stock market funds in 17 of the 25 months since then, withdrawing a net $137 billion, according to Lipper.

Panic Ticks

Thomas Peterffy had seen it all. The Black Monday crash of October 19, 1987, the 1998 collapse of the giant hedge fund Long-Term Capital Management, the implosion of the dot-com bubble in 2000 and 2001, the credit crisis of 2008.

Thomas Peterffy, founder and CEO of Interactive Brokers, has been voicing his opinion about the impact of high-frequency trading on the markets. Jesse Neider for The Wall Street Journal.

But what was unfolding on the afternoon of May 6, 2010 was different. This was fast. This was high-speed trading.

The founder of Interactive Brokers Group Inc. and Timber Hill, a sophisticated computer-driven trading operation, was monitoring the market from a private study on his luxurious estate in Greenwich, Conn.

Chaos was breaking out amid a burst of riots on the streets of Athens, Greece. Stocks had been on their heels all day. But now things were getting much worse. Down about 2% at 2:30 p.m. Eastern, the market had started to plunge rapidly.

Mr. Peterffy picked up the phone and called Timber Hill’s trading desk, several miles away in downtown Greenwich.

«What the heck is happening?» he said.

«Don’t know,» a rattled trader replied.

«Well find out!» Peterffy shouted.

As the Timber Hill traders scrambled to find the cause of the problem, they started seeing a wave of «panic ticks» on their screens—warning signs indicating that their positions were moving so rapidly that they were risking big losses.

By 2:40 p.m., the number of panic ticks exploded. Mr. Peterffy called the trading desk again to see if anyone knew what was happening.

No one did.

Tradebot

In a bland, cube-shaped building on the outskirts of Kansas City, Dave Cummings watched from his corner office as the stock market unraveled like a ball of yarn.

Dave Cummings, Tradebot’s founder Reuters.

The founder of Tradebot Systems, one of the world’s most advanced high-frequency trading operations, wasn’t sure what to make of the downward draft. The heavy volume was scrambling trading systems, leading to disparities in prices quoted on various exchanges. The decline became so sharp that it made Mr. Cummings worry that it wasn’t going to right itself.

Like many others, he worried that a «fat finger» mistake by a trader—Wall Street slang for someone who pressed the wrong button or put too many zeros into a sell order—had triggered a cascade that was turning into a vicious feed-back loop.

If there was an erroneous trade, that meant Tradebot’s systems, which tracked all corners of the market for signals about future conditions, were operating on bad information. If Tradebot kept trading, it might spread the turmoil elsewhere, like a contagious virus.

Digitalized and Decimalized

As the stock market plunged, then Senator Ted Kaufman (D., Del.) was presiding as chair of the Senate. A wave of chatter rippled through the chamber as the senators, clicking on their handheld devices, stared in amazement at news of a major crash in the stock market.

Mr. Kaufman had been one of the fiercest critics of the computer-driven machines that had taken over the market. But he never thought he would see anything like what had just occurred.

Addressing his colleagues from the floor, he explained how the market had shifted from a floor-based system to one that was «digitalized and decimalized.»

«People came into the market and began to develop these high-speed computers,» he said. «Human beings were no longer doing the trading, computers were. They developed these algorithms. It ran automatically. It grew and grew. There is no way to know what is going on. No one knows what is happening in these exchanges when this trading is going on. We have a very dangerous situation.»

Pools of Darkness

In the weeks and months following the flash crash, a fierce debate erupted over what had become of the stock market. Angry words were exchanged in the halls of Capitol Hill, on financial television shows and at trading firms in New York and Chicago.

Congress held panel discussions. The Securities and Exchange Commission grilled the previously unknown chieftains of the high-speed merchants, including Mr. Cummings of Tradebot and Mr. Peterffy of Timber Hill.

The complex, labyrinthine nature of the market vexed ordinary investors. Years ago, before the rise of electronic networks, most trading took place at the New York Stock Exchange and Nasdaq.

BY 2012, trading occurred in roughly seventy different venues, including giant hedge funds and banks. So-called «dark pools,» private markets in which trading took place away from public exchanges such as the NYSE, accounted for more than 10% of all U.S. stock trades, according to Tabb Group.

As the markets slid into discrete pools of darkness, investors, too, had been left in the dark.

Did Donald Trump defraud thousands who paid up to $35,000 to learn his real-estate investing skills at the now defunct Trump University, as New York attorney general Eric Schneiderman charges? Or—ahem—is Schneiderman, in cahoots with President Obama, out to get Trump?

TRUMP L’OEIL “I got a picture of myself with a Trump cutout and … little else,” says Bob Guillo, who paid $35,000 for seminars.

Donald J. Trump has 2.43 million followers on Twitter, making him the 670th most followed person in the global Twitterverse. Last fall he was sandwiched there between Lonny Rashid Lynn Jr., better known as the Chicago-born hip-hop artist Common, and Alejandro Fernández, or El Potrillo, the Mexican singer.

The Donald likes to tweet about his many triumphs and to re-tweet exhortations for him to run for president and save the country. On October 29, he re-tweeted a boast from his daughter Ivanka—who has more than 1.5 million followers—that the yet to be completed Trump International Golf Club, in Dubai, was voted by the International Property Awards “the Best Golf Development in the Middle East.” That same day, he revealed that his Virginia winery had been awarded the “coveted” Virginia Double Gold Medal.

One project The Donald isn’t crowing about on Twitter—or anywhere else, for that matter—is the public-relations problem known first as Trump University and then as the Trump Entrepreneur Initiative, his effort to teach the great unwashed (for as much as $35,000 a head) his vaunted investing techniques. If Eric Schneiderman, the New York attorney general, is to be believed, this particular (now defunct) Trump enterprise was nothing short of out-and-out fraud. Touré, a host of The Cycle on MSNBC, appears to agree. He tweeted to The Donald, “Why did you rob all those Trump University students out of their money?”

Schneiderman thinks that’s a good question, and he wants a good answer. Last August the attorney general’s office filed suit against Trump and his associates for more than $40 million in New York State Supreme Court, claiming that between 2005 and 2011 they “intentionally” misled “over 5,000 individuals nationwide,” including some 600 New York State residents, who paid to “participate in live seminars and mentorship programs with the promise of learning Trump’s real estate investing techniques.” Schneiderman asserted that Trump personally made about $5 million from the endeavor—although Trump said he intended to donate any profits to charity. (Now he says that between legal fees and refunds no money is left to do so.)

At a press conference announcing the suit, Schneiderman claimed that “Mr. Trump used his celebrity status and personally appeared in commercials making false promises to convince people to spend tens of thousands of dollars they couldn’t afford for lessons they never got.”

Trump wasted little time in responding, hitting the airwaves to call into question Schneiderman’s character—he’s a “political hack,” Trump told Fox & Friends—and his motivation for filing the suit. Trump claims that Schneiderman cooked up the lawsuit after visiting with President Obama—the target of much of Trump’s political ire (recall Trump’s birther non-bombshell)—in upstate New York. They met on a Thursday and Schneiderman filed the lawsuit that Saturday, leaving Trump incredulous. “It’s a helluva coincidence,” he tells me. “You meet and then you immediately file a lawsuit and the lawsuit is filed not on a Monday or Tuesday but on a Saturday?… I’ve had a lot of litigation. I have never heard of a lawsuit being filed on a Saturday.”

Schneiderman responds, “I assure you I have many more important things to talk to the president about than the fact that we busted this penny-ante fraud… [Trump] seems to be the kind of person who goes to the Super Bowl and thinks the people in the huddle are talking about him.” As to why the suit was filed on a Saturday, Schneiderman says that Trump and his attorneys asked him to hold off until the weekend, allowing Trump to leak in advance his side of the story to the Saturday editions of the New York Post and The Wall Street Journal and “to whip up this strange Web site attacking me.”

Trump says Schneiderman came to him hat in hand for a campaign contribution in 2010, when he was thinking about running for office. On one of the three visits that Trump alleges Schneiderman made, Trump gave him $12,500: “He said, ‘Can you fix me up with some people?’ I set him up with people. Now you can make the case ‘Isn’t that wonderful that there’s somebody who helped him that he’ll screw.’ But you could also say he’s a real disgusting human being.”

Trump elaborated in a recent letter to Graydon Carter, the editor of Vanity Fair: “He wanted to settle and I didn’t… During settlement negotiations, he was asking for campaign contributions. He’s a sleazebag and a crook who is driving business out of New York City.” To Trump’s charges, Schneiderman responds, “The fact that he has a larger megaphone than most fraudsters is what gets all the attention here, so I would expect that he would attempt to distract the court, unsuccessfully…. It is true that he did not support me in the Democratic primary when I ran in 2010, and, after I won the primary, he gave me one contribution, which is the only contribution he has ever given me.”

Schneiderman fought back with an opinion piece in the Daily News, as well as with numerous TV appearances. “Trump has answered with outlandish accusations,” he wrote. “That’s not surprising for a showman who has built a career around bluster and hype. But I am not in the entertainment business; I am in the justice business.” He conceded that Trump could have settled the case—as another for-profit school did for $10 million—“or answered the charges in a dignified manner through his attorney. Instead,” the attorney general continued, “he chose to try the case in the press.”

‘I went to the Wharton School of Finance,” Trump says. “I have a great feeling for education and for knowledge and learning… I love the idea of helping people, because I’ve had a lot of experience with real estate, to put it mildly.”

Trump and his associates Michael Sexton and Jonathan Spitalny formed Trump University as a limited-liability corporation in 2004. The original business plan was to focus on long-distance, Web-based learning, but they would also be “experimenting” with offering “live instructional programs” to paying customers, according to Sexton’s subpoenaed deposition.

The following spring, the New York State Department of Education sent letters to both Trump and Sexton notifying them that Trump University was in violation of state law by calling itself a “university” when “it was not chartered as such” and because it had not been properly “licensed” by the state.

In a series of follow-up conversations and e-mails between Sexton and Joseph Frey, then a state education official, Frey explained that Trump University could avoid the “licensure” provision of the state law if it were to re-incorporate outside of New York State and if it ran no physical seminars in the state. But “Trump University failed to abide by any of these conditions,” the attorney general wrote.

Schneiderman claims the “university” continued to use 40 Wall Street—one of the few buildings in Manhattan that Trump actually owns—as its principal corporate address, including in numerous advertisements. It furthermore conducted “at least fifty live programs in New York between 2006 and 2011.” Schneiderman noted that “Trump University LLC” was finally renamed, on May 20, 2010, “The Trump Entrepreneur Initiative LLC.”

In his deposition Sexton admitted that the failure to comply with the stipulations was “an oversight” and something he and Trump “forgot” about.

Also misleading, according to Schneiderman, were the claims made in Trump’s advertising. In one, published in 2009, Trump looks resplendent in a blue suit while standing in front of one of the buildings that bear his name—but not his ownership—on Manhattan’s West Side. “Learn from Donald Trump’s handpicked experts how you can profit from the largest real-estate liquidation in history,” the ad promises. (He was presumably not referring to the Chapter 11 filings of the three highly leveraged hotel and casino properties he once had a stake in.) The ad pronounced Trump “the most celebrated entrepreneur on earth. He’s earned more in a day than most people do in a lifetime… And now he’s ready to share—with Americans like you—the Trump process for investing in today’s once-in-a-lifetime real estate market.”

This was followed by a quotation from The Donald: “I can turn anyone into a successful real estate investor, including you.”

Schneiderman argues that Trump University’s advertisements, Web site, and promotional materials were just an elaborate ruse. The initial “free seminars,” according to the lawsuit, were “the first step in a bait and switch to induce prospective students to enroll in increasingly expensive seminars starting with the three-day $1495 seminar and ultimately [for] advanced seminars such as the ‘Gold Elite’ program costing $35,000.”

“We’re going to have professors that are absolutely terrific—terrific people, terrific brains, successful, the best,” Trump claimed on videos shown at the seminars. “We’re going to have the best of the best. And honestly, if you do not learn from them, if you do not learn from me … then you’re just not going to make it in terms of the world of success.”

That was good enough for June Harris, of White Plains, New York, who had previously taken an online Trump real-estate investing course and found it useful. After the free June 2009 session at a hotel in Stamford, Connecticut—where participants were told to keep $1,000 in their pockets at all times as “a confidence builder for wealth”—Harris signed up for the three-day seminar, which cost her $747.50. She spent the weekend of June 19 at the seminar, where she was encouraged to call her credit-card company and increase her line of credit. “They said that we should invest in property without ever touching our own assets,” she wrote in a September 2012 affidavit. “The instructor said if we surmounted the fear of losing money then we would actually make money.”

She was then encouraged to sign up for the “Trump Gold” mentorship program—at a cost of $35,000—described as a yearlong group of seminars and private consultations with Trump instructors. When Harris declined, “The agent was very upset and quickly hung up the phone on me,” she wrote in her affidavit.

Bob Guillo, from Manhasset, New York, and his son, Alex, fell hard for the Trump line. After the free seminar and the three-day course costing nearly $1,500—and which he graded as “excellent” in his evaluation—Guillo signed up for the Trump Gold Elite program and paid nearly $35,000. He was told he would be part of a select “in-the-know group” and among “insiders” who would have access to proprietary real-estate deals. “For example,” Guillo wrote in an affidavit, “where Mr. Trump would be involved in building condominiums, we would get first choice at purchasing an apartment and then would be able to immediately sell it at a profit.”

Guillo wrote that at the first day of the Trump Gold Elite program he “began to realize I had been taken” because the information conveyed seemed to be coming from Zillow.com, a real-estate Web site, or from the I.R.S. Web site. In August 2011, Guillo wrote George Sorial, an assistant general counsel in the Trump Organization, to request a refund. But he never got his money back. Instead, “Trump staff promised to set me up with their best mentor,” Guillo wrote. He declined the offer. He just wanted his money back.

Guillo, now 74 years old and a retired legal-document processor, says he attended every one of the seminars his $35,000 bought him and at every one the Trump instructors did the same thing. “They tried to solicit more money from us,” he explains. “I got a picture of myself with a Trump cutout and basically very, very little else.”

Trump is unmoved by the people who have complained. He and his legal advisers set up a Web site, 98percentapproval.com, which contains video testimonials from satisfied customers, as well as more than 10,000 attendee surveys, many of which give Trump top marks. “It’s like Harvard,” Trump tells me. “You know Harvard doesn’t have a 98 percent approval rating.” Alan Garten, an executive vice president of the Trump Organization and litigation counsel, interjects, “When you take into account the fact that the attorney general’s been looking at this case for what, two-plus years, 46 [negative] affidavits is [nothing].”

Trump quickly picks up on Garten’s observation. “Of those 46,” The Donald says, “most of them have signed a letter saying how great it was… They complained that they weren’t given refunds, except they were.”

What about Bob Guillo, who has not received a refund? “I had many conversations with Bob Guillo,” says Sorial. “He could not articulate one thing that was wrong with the course. And I just got the impression that this was a guy who read about this frivolous lawsuit and was saying, ‘Hey, look. I’m going to try and get some money back.’ Especially because he signed up for multiple courses in multiple years, and had multiple, very positive evaluations.”

Schneiderman is not persuaded by such arguments. “All the promotional materials, many of which featured Mr. Trump, made numerous false statements,” he explains. “He never ‘handpicked’ experts to teach people. These people weren’t experts. They weren’t even certified as teachers by the state of New York. They didn’t learn any real-estate secrets from Trump, because he never participated in developing the curriculum.” (Trump says he personally reviewed the résumés of many but not all of the teachers.)

Trump is especially miffed that he is being tarred as a fraud. “I really did this because I thought we could really help a lot of people, and we did help a lot of people.” He is determined to make the attorney general pay politically for his accusations and says his legal response “will blow Schneiderman out of the water.”

Schneiderman responds, “I have no idea how he thinks his strategy is going to work.” He adds, “The lawyers in my office are going to pursue it. I am quite confident we’re going to prevail, and the rest of it is just distraction.”

The Bad Brunch – National Underwriter’s 2013 Rogue’s Gallery

The life and health insurance industry, as we’ve seen in 2013, has had its own share of general business problems, aside from any man-made issues such as acts of fraud or a failed website. Like an unsuspecting outlier out to harm an industry working for the physical and financial health of society, these Rogues — either intentionally or unintentionally — have caused some of society to form a different view of an industry constantly trying to better its reputation.

By Emily Holbrook, Bill Coffin, Allison Bell, and Warren S. Hersch

Artwork by Tim Foley Illustrations

#10

James A. Guest

James A. Guest, the CEO and president of Consumer Reports, was an insurance commissioner in Vermont back in the 1970s. At Consumer Reports, he’s been part of an organization that’s pushed for tough insurance product and insurance sales practices standards for decades.

Guest has earned a spot on the list for being a representative of some of the groups that claim to speak for consumers but lost their tongues when federal officials did a questionable job of implementing the Patient Protection and Affordable Care Act (PPACA) programs.

This year, Consumer Reports’ lobbying arm, Consumers Union, along with other advocacy groups, have lobbied hard against imposing tough training or disclosure standards on “their reps” — PPACA exchange navigators.

Consumers Union told the Obama administration in May that federal agencies should set uniform navigator standards; that navigators should not get paid by agents, brokers or stop-loss insurers; and that the U.S. Department of Health and Human Services should “actively monitor and intervene, as necessary, to ensure that state licensing, certification and other requirements do not interfere with navigators’ abilities to fulfill all of their legal responsibilities.”

We thought of comparing the Consumer Reports stance on navigators with its approach to the sudden, nightmarish curtailment of PPACA Preexisting Condition Insurance Plan benefits that took place earlier this year. In other words, the shafting of consumers who are in the middle of getting organ transplants.

We looked for some policy statement expressing Consumer Reports’ or Consumers Union’s outrage toward this and found a February brief urging individuals to “Act fast to get this health reform benefit.” No expression of outrage, not even an expression of mild sorrow, just advice to those slowpokes with iron lung machines to move it with the paperwork already.

#9

Hugh R. Hinsinger, Jr.

Hugh R. Hinsinger, Jr. worked as a financial advisor and was entrusted with many clients’ finances, including those of his parents. But Hunsinger, 49, of Pine Brook, New Jersey, was not interested in his fiduciary responsibility. Greed was the only thing on his mind.

In August, Hunsinger pleaded guilty to second-degree theft by unlawful taking after it was revealed that he defrauded his parents out of more than $1.3 million while serving as their financial advisor.

According to the Financial Industry Regulatory Authority, Hunsinger told his parents that he was selling securities they owned to invest in new insurance or securities products. Instead, Hunsinger deposited the funds into bank accounts he controlled. The complaint also alleges that Hunsinger recommended that his parents invest in a deferred combination variable and fixed annuity. Hunsinger, formerly of Lincoln Financial Advisors Corporation, provided his parents with documents that contained information, based on a historical illustration, concerning withdrawals, contract values, cash surrender, average annual returns and standard death benefit. Hunsinger sold the securities in the account but never bothered to purchase the annuity.

“For years, the victims in this case believed that their son was investing money on their behalf,” acting state Attorney General John Hoffman said in a statement. “Instead, he was siphoning their money for his own benefit.”

Under the plea agreement, the state recommended that Hunsinger be sentenced to three to five years in state prison and that his insurance producer license be suspended for a period of five years. Hunsinger will also be required to pay back $1,354,496 to his parents. For his sheer lack of heart and morals, Hunsinger justly earns the number nine spot on our list.

#8

All State Insurance

In July, Allstate sold its Lincoln Benefit Life to Resolution Life, a British financial services firm, for $600 million. With this move, Allstate essentially abandoned the consumer segment served by independent life insurance and annuities agencies. Allstate promoted the sale to Resolution Life Holdings as a benefit, as the firm estimated it would reduce required capital in Allstate Financial by approximately $1 billion.

Some in the industry, however, viewed it as a less-than-ethical maneuver, feeling as though Allstate sold off a perfectly good, profitable division to a company they knew would liquidate it instead of selling to a buyer who would keep it going. Many at Allstate believed Lincoln Benefit to be a great unit, and many of their people were bewildered at why Allstate would do this. One insider, who confided in National Underwriter off the record, felt that Allstate didn’t have to handle it the way they did and that there were alternatives that would have prevented shuttering the division — and laying off employees in the process.

In September, the Florida Department of Health blew the chance of calmly trying to bring order to the “Wild Exchange West” by sending out a memo telling local health department directors to keep exchange navigators away from county health department offices. Department officials first said the order went out because county health departments lack the space to provide the navigators with privacy-protecting private offices. But the reasons the department used to justify the memo seem to have evolved over time, while FlaglerLive and Health News Florida never found evidence the department had sent out similar memos concerning similar outreach efforts.

Whatever the true reasons for the memo were, it surfaced at an awkward time and seems to have encouraged the possibility of getting consumer groups to think harder about exchange consumer protection issues further into the future.

And, by the way, like Consumer Reports, which earned a mention in our Rogue’s list by seeming to care too little about navigator standards, the Florida Department of Health was pretty quiet about the abrupt curtailment of PPACA Preexisting Condition Insurance Plan benefits earlier this year.

The message: Helping consumers fill out an exchange plan application in a county health department lobby is a terrible idea, and forcing a man who’s about to get a liver transplant to find a new surgeon and accept a higher out-of-pocket spending maximum is quite the bore.

#6

Richard Allen Freer

Richard Allen Freer, of Palmer Township, Pennsylvania, was once the president of a local bank, and then a rep for Aviva before he struck out on his own as a financial advisor. But that all came crashing down when Northampton County District Attorney John Morganelli charged Freer with 272 different counts related to a Ponzi scheme he ran for the last 15 years, bilking 82 different clients — some of them friends — out of some $10 million.

One victim, Joan Curto, a widow whose 80-year-old husband died two years ago, said Freer attended her husband’s viewing and visited her home the day he died — all while pocketing the money due to her. Curto has a few choice words for Freer, should she ever encounter him again: “What does it profit a man to gain the whole world, only to suffer the loss of his own soul?”

Local papers took Freer’s case as cause to raise a skeptical eyebrow at the larger financial services industry, and to suggest that Ponzi schemes could be lurking behind any corner. Freer is currently being held in general population in Northampton County Prison, and DA Morganelli has made it clear that he hopes Freer will die there.

Freer is still innocent until proven guilty in a court of law, but it does not look good for him at the moment. His spot on this list is for the disrepute his actions have already brought upon all financial advisors; if he is convicted next year, he can expect a higher place on this list. And if he is found innocent? Then Morganelli gets his spot.

#5

Ben Lawsky

Mr. Lawsky earns the number five spot for his lack of leadership at the helm of New York’s Department of Financial Services (DFS). His department levied hundreds of millions of dollars in fines to various lawbreakers, and then watched the money all dump into the state’s general treasury fund (read: Andrew Cuomo’s Presidential Campaign war chest). Cuomo and Lawsky go way back and Cuomo has made clear his strong desire to run for president in 2016, while Lawsky is nothing short of a willing pawn in Cuomo’s political passion. Many see Lawsky’s aggressiveness as an attempt to undermine New York Attorney General Eric Schneiderman, Cuomo’s successor.

All this while Lawsky allowed the structured settlement annuity holders from the Executive Life Insurance Company of New York debacleto endure unjust financial ruin while the state approved of the company’s draconian liquidation plan. And has Lawsky held anyone at the New York Liquidation Bureau accountable? Of course not.

Meanwhile, remember Superstorm Sandy? According to one source, Lawsky failed to remove the department’s records on insurers from the DFS’s flood-prone office in lower Manhattan, so when the tides rushed in, the records were destroyed. When you can’t be bothered to keep hundreds of innocent families from being destroyed financially, moving boxes of paper are probably low on the priority list, as well.

#4

Rachel Abelson

In 2008, producer Glenn Neasham sold an annuity to 83-year-old Fran Schuber of Lake County, California, who was later revealed to be suffering from early stages of dementia at the time of the transaction. California law allows for annuities to be sold to clients as old as 85 and Schuber’s annuity resulted in a $40,000 profit for his client. And as far as Neasham could tell, his client was lucid at the time of sale.

None of this prevented Lake County District Attorney Rachel Abelson from throwing the book at Neasham, however. He was arrested in 2010 and charged with a felony count of theft from an elderly individual. In 2011, he was sentenced to 90 days in jail with three years probation. His insurance license was revoked, his income fell to just $20,000 annually and his family lost their house and were forced to live off food stamps.

Neasham appealed the verdict and went free on bail pending that appeal, and ultimately, in October of this year, his charges were reversed. But it destroyed his practice, cost him a fortune in legal fees, and put him squarely in the “guilty until proven innocent” box. Abelson undoubtedly saw her actions as trying to protect Lake County’s large elderly population. But destroying a man innocent of any crimes on incomplete evidence isn’t the way to do it.

#3

Ben Bernanke

Ben Bernanke’s term as Federal Reserve chairman comes to an end January 2014. From the life insurance industry’s perspective, his departure is long overdue.

As Fed chief, Bernanke presided over a long run of abysmally low interest rates and companies have found it increasingly difficult to make money on hedging strategies sufficient enough to make good on living benefit guarantees, most notably with variable annuities.

Result: Profit margins have suffered, forcing companies to revamp their products by offering less generous guarantees and/or charging more for them. In some cases, insurers have felt compelled to jettison once profitable business lines.

To be sure, low interest rates aren’t solely to blame for insurers’ woes. Yet, life insurers and the analysts that track their financials consistently cite low interest rates as the chief macroeconomic threat to the businesses. And so Fed Chairman Bernanke has consistently drawn the industry’s ire.

Many say the criticism is unjustified, believing the Fed’s quantitative easing has effectively counteracted fiscal policy guided by a misplaced focus on reining in federal deficits. Point noted. But the fact remains that financial services companies will continue to be handicapped so long as interest rates remain artificially low. And for that, Mr. Bernanke remains a veteran Rogue.

#2

John Boehner

The beleaguered Speaker of the House became the face for Republican opposition to Obamacare when the GOP took control of the House during the 2010 midterm elections. But what has he managed to accomplish since then, especially on behalf of those in the business community most angered by PPACA’s passing? Not much.

The government shutdown in October, which has been an unmitigated disaster for Republican approval ratings and for their ability to collectively negotiate with the Obama administration, was the work of a Tea Party contingent Boehner proved powerless to wrangle. For those in the health insurance industry who stand opposed to PPACA, all Boehner did was convince people that PPACA was no longer a battle worth fighting, that the Republicans were a spent force, and that Democrats could already begin to look forward to 2016.

There are those who have suggested that Boehner hoped the Tea Party might exhaust itself fighting PPACA, and once spent, the rest of the GOP could get back to work advancing its priorities on other fronts. If so, that’s a decent play to make, but a risky one. The Tea Party is a passion movement, uninterested in dealing itself in to the traditional Washingtonian power channels. Any deals made with them are done at the deal-maker’s risk, which Boehner now knows only too well.

#1

HealthCare.gov

There is no individual or organization that deserves the number one spot more than the federal health care exchange website HealthCare.gov.And we must note that President Obama, Department of Health and Human Services Secretary Kathleen Sebelius and Centers for Medicare and Medicaid Services Administrator Marilyn Tavenner also share in this infamous award.

Not long after the official Oct. 1 open enrollment date, those involved with the site — and users looking to sign up — began reporting problems. In fact, it was reported that only three in 10 applications started actually reached completion.

In late October, at a hearing organized to analyze the problems faced by the federal exchange, Officials of CGI and Optum/QSSI, two of the key vendors, admitted that months of end-to-end testing — not the days or last two weeks before launching — is the industry standard for a complex website being used to solicit applications for insurance policies.

The Republicans claimed that almost $175 million in funding was more than enough to build a successful site, while the Democrats claimed that Republicans sabotaged the site by pressuring states to refuse to build their own online marketplace, steering consumers instead to the federal one, which was not built for such a customer size. Then, as if bugs within the website weren’t enough, the administration was faced with security issues involving the site, especially after reports surfaced of one applicant’s personal information being shared with another applicant. The failed site drew so much criticism from consumers, politicians and even PPACA supporters that the chief information officer for the CMS, Tony Trenkle, resigned in November.

In essence, the administration is attempting to run the biggest startup in the world, without having anyone on board who has run a startup, let alone a business.

A true history of fraud would have to start in 300 B.C., when a Greek merchant name Hegestratos took out a large insurance policy known as bottomry. Basically, the merchant borrows money and agrees to pay it back with interest when the cargo, in this case corn, is delivered. If the loan is not paid back, the lender can acquire the boat and its cargo.Hegestratos planned to sink his empty boat, keep the loan and sell the corn. It didn’t work out, and he drowned trying to escape his crew passengers when they caught him in the act. This is the first recorded incident as of yet, but it’s safe to assume that fraud has been around since the dawn of commerce. Instead of starting at the very beginning, we will focus on the growth of stock market fraud in the U.S.

The First Insider Trading Scandal

In 1792, only a few years after America officially became a nation, it produced its first fraud. At this time, American bonds were like developing-world issues or junk bonds today – they fluctuated in value with every bit of news about the fortunes of the colonies that issued them. The trick of investing in such a volatile market was to be a step ahead of the news that would push a bond’s value up or down.

Alexander Hamilton, secretary of the Treasury, began to restructure American finance by replacing outstanding bonds from various colonies with bonds from the U.S. bank. Consequently, big bond investors sought out people who had access to the Treasury to find out which bond issues Hamilton was going to replace.

William Duer, a member of Washington’s inner circle and assistant secretary of the Treasury, was ideally placed to profit from insider information. Duer was privy to all the Treasury’s actions and would tip off his friends and trade in his own portfolio before leaking select info to the public that he knew would drive up prices. Then Duer would simply sell for the easy profit. After years of this type of manipulation, even raiding Treasury funds to make larger bets, Duer left his post but kept his contacts inside. He continued to invest his own money as well as that of other investors in both debt issues and the stocks of banks popping up all over the country. (For more, check out Top 4 Most Scandalous Insider Trading Debacles.)

With all the European and domestic money chasing bonds, however, there was a speculative glut as issuers rushed to cash in. Rather than stepping back from the overheating market, Duer was counting on his information edge to keep ahead and piled his ill-gotten gains and that of his investors into the market. Duer also borrowed heavily to further leverage his bond bets.

The correction was unpredictable and sharp, leaving Duer hanging onto worthless investments and huge debts. Hamilton had to rescue the market by buying up bonds and acting like a lender of last resort. William Duer ended up in debtor’s prison, where he died in 1799. The speculative bond bubble in 1792 and the large amount of bond trading was, interestingly enough, the catalyst for the Buttonwood Agreement.

Fraud Wipes Out a Former President

Ulysses S. Grant, a renowned war hero and former president, only wanted to help his son succeed in business, but he ended up causing a financial panic. Grant’s son, Buck, had already failed at several businesses but was determined to succeed on Wall Street. Buck formed a partnership with Ferdinand Ward, an unscrupulous man who was only interested in the legitimacy gained from the Grant name. They opened up a firm called Grant & Ward. Ward immediately went around raising capital from investors, falsely claiming that Ulysses S. Grant had agreed to help them land fat government contracts. Ward then used this cash to speculate on the market. Sadly, Ward was not as gifted at speculating as he was at talking. He lost heavily.

Of the capital Ward squandered, $600,000 was tied to the Marine National Bank, and both the bank and Grant & Ward were on the verge of collapse. Ward convinced Buck to ask his father for more money. Grant Sr., already heavily invested in the firm, was unable to come up with enough, and had to ask for a $150,000 personal loan from William Vanderbilt. Ward essentially took the money and ran, leaving the Grants, Marine National Bank and the investors holding the bag. Marine National Bank collapsed after a bank run and its fall helped touch off the panic of 1884.Grant Sr. paid off his debt to Vanderbilt with all his personal effects, including his uniforms, swords, medals, and other memorabilia from the war. Ward was eventually caught and imprisoned for six years.

The Pioneering Daniel Drew

Moving from fraud, to insider trading, to stock manipulation, the number of examples explodes. The late 1800s saw men like Jay Gould, James Fisk, Russell Sage, Edward Henry Harriman and J.P. Morgan turn the fledgling stock market into their personal playground. However, because we’re giving precedence to the pioneers of fraud and stock market manipulation, we need look no further than Daniel Drew. Drew started out in cattle, bringing the term «watered stock» into our vocabulary – later he introduced this same term to stocks. He became a financier when the portfolio of loans he provided to fellow cattlemen gave him the capital to start buying large portions of transportation stocks.

Drew lived in a time before disclosure, when only the most basic regulations existed. His technique was known as a corner. He would buy up all of a company’s stocks, then spread false news about it to drive the price down. This would encourage traders to sell the stock short. Unlike today, it was possible to sell short many times the actual stock outstanding.

When the time came to cover their short positions, traders would find out that the only person holding stock was Daniel Drew and he expected a premium. Drew’s success with corners led to new operations. Drew often traded wholly-owned stocks between him and other manipulators at higher and higher prices. When this action caught the attention of other traders, the group would dump the stock back on the market.

The danger of Drew’s combined poop and scoop, pump and dump schemes was in taking the short position. In 1864, Drew was caught in a corner by Vanderbilt. Drew was trying to short a company that Vanderbilt was simultaneously trying to acquire. Drew shorted heavily, but Vanderbilt had purchased all the shares. Consequently, Drew had to cover his position at a premium paid directly to Vanderbilt.

Drew and Vanderbilt battled again in 1866 over another railroad, but this time Drew was much wiser, or at least much more corrupt. As Vanderbilt tried to buy up one of Drew’s railroads, Drew printed more and more illegal shares. Vanderbilt followed his previous strategy and used his war chest to buy up the additional shares. This left Drew running from the law for watering stock and left Vanderbilt cash poor. The two combatants came to an uneasy truce: Drew’s fellow manipulators, Fisk and Gould, were angered by the truce and conspired to ruin Drew. He died broke in 1879.

The Stock Pools

Until the 1920s, most market fraud affected only the few Americans who were investing. When it was confined largely to battles between wealthy manipulators, the government felt no need to step in. After WWI, however, average Americans discovered the stock market. To take advantage of the influx of eager new money, manipulators teamed up to create stock pools. Basically, stock pools carried out Daniel-Drew-style manipulation on a larger scale. With more investors involved, the profits from manipulating stocks were enough to convince the management of the companies being targeted to participate. The stock pools became very powerful, manipulating even large cap stocks like Chrysler, RCA and Standard Oil.

When the bubble burst in 1929, both the general public and the government were staggered by the level of corruption that had contributed to the financial catastrophe. Stock pools took the lion’s share of the blame, leading to the creation of the Securities and Exchange Commission (SEC). Ironically, the first head of the SEC was a speculator and former pool insider, Joseph Kennedy.

The SEC Era

With the creation of the Securities and Exchange Commission (SEC), market rules were formalized and stock fraud was defined. Common manipulation practices were outlawed, as was the large trade in insider information. Wall Street would no longer be the Wild West where gunslingers like Drew and Vanderbilt met for showdowns. That isn’t to say that the pump and dump or insider trading has disappeared. In the SEC era, investors still get taken in by frauds, but they have now have legal protection that makes it possible for them to at least get some satisfaction.

A.M. Best Affirms Ratings of National Western Life Insurance Company

A.M. Best Co. has affirmed the financial strength rating of A (Excellent) and issuer credit rating of «A» of National Western Life Insurance Company (NWL) (Denver, CO) [NASDAQ: NWLI]. The outlook for both ratings is stable.

The affirmation of the ratings reflects NWL’s stable statutory capital and surplus and consolidated GAAP equity, its strong level of risk-adjusted capitalization, profitable net operating performance–albeit decreased in 2011 due to index option volatility–the absence of financial leverage in its capital structure and a conservative fixed income investment portfolio. The rating actions also reflect NWL’s diverse business profile, which includes dollar-denominated life products to residents of Latin and Central America countries. A.M. Best recognizes NWL’s long-standing presence in the international life insurance segment as a strong competitive advantage that provides diversification of revenue, earnings and risk management. Other positive rating factors include NWL’s well-defined hedging programs designed to mitigate the equity market risk associated with its fixed index annuities and life products and asset/liability management that ensure appropriate matching of its assets with its product liabilities.

Partially offsetting these positive rating factors is NWL’s large and increasing exposure to interest-sensitive liabilities, which is a result of recent strong growth in annuity sales. The company’s interest-sensitive liability growth trends are supported primarily by a fixed-income investment portfolio, which could be vulnerable to declining yields and further reinvestment risks. A.M. Best recognizes that these risks are somewhat mitigated by surrender charge protection and market value adjustments within its annuity products, as well as by its strong capital position. A.M. Best believes NWL may be challenged to sustain and improve its historical operating performance given the expense strains expected from anticipated new business growth, the challenges of increased competition and costs related to its continuing technology enhancement initiatives. While acknowledging its recent efforts to grow its U.S. domestic life businesses, A.M. Best believes the company will remain challenged to meaningfully grow this segment in the near term given the intense competitive landscape of the individual life insurance market.

A.M. Best believes NWL is well positioned at its current ratings. Downward rating pressure could occur if there is a continuing trend of declining statutory earnings or sizable operating losses, further product concentration risk from the company’s interest sensitive liabilities and a significant drop in its reported risk-adjusted capitalization.

The methodology used in determining these ratings is Best’s Credit Rating Methodology, which provides a comprehensive explanation of A.M. Best’s rating process and contains the different rating criteria employed in the rating process. Additional key criteria utilized include: «Understanding BCAR for Life and Health Insurers»; «Assessing Country Risk»; and «Risk Management and the Rating Process for Insurance Companies.» Best’s Credit Rating Methodology can be found at www.ambest.com/ratings/methodology .

Founded in 1899, A.M. Best Company is the world’s oldest and most authoritative insurance rating and information source. For more information, visit www.ambest.com Fuente: A.M. Best Company, Inc. 31/05/12.

Cómo la salida a bolsa de Facebook pasó de estelar a bochornosa

Por Gina Chon, Jenny Strasburg y Anupreeta Das

Capital Research & Management quería comprar acciones de Facebook Inc. durante su salida a bolsa. No obstante, días antes de la oferta pública inicial, un banco colocador le advirtió a la firma de inversión sobre las menguantes perspectivas de ingresos de la red social.

La firma de Los Ángeles, que contaba con información de una reunión del 11 de mayo durante la gira promocional con entidades colocadoras y Facebook, así como estimaciones similares propias, redujo la cantidad de acciones que pretendía adquirir. La noche anterior al debut bursátil, un gestor de Capital Research le dijo a un banquero de Morgan Stanley, el principal colocador, que el precio de salida era «ridículo», según una persona al tanto de la situación. Algunos gestores de fondos de Capital Research prefirieron no participar en la salida a bolsa de Facebook, dicen fuentes al tanto.

Jennifer Kohne no recibió tal advertencia. La representante de ventas de 52 años, que vive en St. Louis, compró 3.000 acciones de Facebook el viernes a US$42 a través de una corredora en línea y ahora acumula pérdidas de cerca de US$30.000, según el precio de cierre del miércoles de US$32.

«No recibimos la información que estos gestores de fondos institucionales obtienen», se lamenta. «Estamos en desventaja».

Es uno de los secretos mejor guardados de Wall Street: a las firmas de valores se les permite conversar con grandes clientes de inversión sobre información crucial mientras preparan salidas a bolsa.

Las firmas de Wall Street, por su parte, afirman que dan cierta información a grandes clientes porque pagan por este tipo de datos. Es normal en una salida a bolsa que los analistas o el personal de ventas brinde determinada información a clientes, agregan. Pero, en general, la práctica no abarca a pequeños inversionistas.

En cualquier otra instancia, tal «divulgación selectiva» violaría las leyes bursátiles de Estados Unidos, que exigen que las empresas y las firmas de Wall Street difundan públicamente cualquier información que podría afectar los precios de las acciones. Las normas de valores prohíben que analistas de bancos que colocan grandes salidas a bolsa publiquen informes de investigación hasta 40 días después de que las acciones empiecen a negociarse.

Algunos abogados de valores piden que se implementen nuevas reglas para evitar este flujo de información desigual. «Los analistas no deberían dar opiniones sobre la salida a bolsa en el momento en que sus firmas están actuando como colocadores. No deberían dar información que no esté en el prospecto para favorecer a clientes», sostiene Jacob Zamansky, abogado que representa a inversionistas en casos de valores. No está involucrado en ninguna causa vinculada a Facebook.

La red social no quiso hacer comentarios. En un comunicado, Morgan Stanley señaló que «siguió los mismos procedimientos para la oferta de Facebook que en todas las salidas a bolsa. Estos procedimientos cumplen con todas las regulaciones pertinentes».

El debut bursátil de Facebook debería haber sido un momento culminante para la red social, Morgan Stanley y el Nasdaq. En cambio, la deslucida oferta inicial —las acciones de Facebook han caído cerca de 16% desde su debut el viernes— ha ilustrado cómo algunas partes del mundo financiero favorecen a los más poderosos.

Las repercusiones han demorado en llegar. Reguladores de estados y de la industria financiera están investigando si hubo irregularidades en las comunicaciones para los inversionistas. El miércoles, algunos accionistas de Facebook presentaron una demanda en la corte federal de Manhattan acusando a la empresa y sus colocadores de no divulgar adecuadamente los cambios que hicieron los bancos en los pronósticos de sus analistas. Asimismo, un comité bancario del Senado examinará lo que sucedió en el proceso de salida a bolsa de Facebook.

Morgan Stanley indicó que podría ajustar los precios de transacciones realizadas durante la salida a bolsa. El banco está revisando órdenes de clientes de corretaje particulares una por una y hará ajustes si pagaron demasiado, según una persona al tanto. En un mensaje enviado el miércoles a casi 17.000 asesores financieros de su empresa conjunta de corretaje minorista Morgan Stanley Smith Barney, la firma señaló que espera realizar «un número» de ajustes de precios. Los pedidos en cuestión ocurrieron durante el debut de Facebook el viernes, que se vio afectado por fallas en el mercado Nasdaq que retrasaron el comienzo de las operaciones por 30 minutos.

Clientes de Morgan Stanley y otras corredoras también tuvieron órdenes que fueron procesadas de forma incorrecta. Más allá de las fallas, algunos inversionistas están enojados porque Facebook elevó el precio de salida a bolsa a US$38 por acción pese a las débiles previsiones para sus ingresos.

Los principales colocadores, que incluyen a Morgan Stanley, Goldman Sachs Group Inc. y J.P. Morgan Chase & Co., fijaron el mejor precio basado en la demanda que vieron el jueves por la noche, dicen fuentes al tanto. Goldman y J.P. Morgan tenían una influencia limitada en la salida a bolsa de Facebook, según personas al tanto. Los tres bancos no quisieron hacer comentarios.

Un alto ejecutivo de Nasdaq dijo el martes a corredores que los ejecutivos de la bolsa «lamentan sinceramente lo que sucedió el viernes» y que ésta no puede evaluar las pérdidas de clientes minoristas individuales pero está trabajando con operadores que están buscando compensación para ellos.- —Susan Pulliam y Aaron Lucchetti contribuyeron a este artículo. Fuente: The Wall Street Journal, 24/05/12. ——————————————————-

En Goldman Sachs, un menú para ganar con la crisis global

Por Susan Pulliam y Liz Rappaport

Uno de los principales estrategas de Goldman Sachs Group Inc. ha distribuido entre cientos de fondos de cobertura, todos clientes de la firma, un análisis bastante sombrío sobre la economía. Esto es bastante común entre las firmas financieras. Lo que llama la atención es que junto a la perspectiva económica, el mismo estratega hace sugerencias sobre formas de sacar ventaja de la crisis financiera de Europa.

En el informe de 54 páginas enviado a los clientes institucionales de Goldman con fecha del 16 de agosto, Alan Brazil, un estratega de la firma que forma parte de la división de corretaje, argumenta que puede necesitarse hasta un billón de dólares (millón de millones) en capital para apuntalar los bancos europeos, que las pequeñas empresas en Estados Unidos —que en el pasado eran un generador de empleo— todavía languidecen y que el crecimiento de China no puede ser sostenible.

Entre las ideas de Brazil para negociar aprovechando la mala perspectiva están: una opción que ofrece una forma de tomar una posición que apuesta a la caída del euro y otra apuesta bajista por medio de un índice de contratos de seguro sobre el crédito de los títulos financieros europeos. El informe también incluye información detallada sobre instituciones financieras europeas y un lenguaje mordaz sobre la profundidad de los problemas en Europa, EE.UU. y China.

Un portavoz de Goldman Sachs expresó: «Por norma, las instituciones financieras publican informes que sugieren estrategias a la medida de las necesidades de sus clientes. Si los clientes buscan cubrir riesgos existentes o tomar posiciones en el mercado cortas o largas, nuestro objetivo es ayudarlos a enfrentar los retos de los mercados actuales». A través del portavoz, Brazil declinó hacer comentarios.

El informe sale a la luz cuando Goldman y sus principales rivales compiten por el negocio de la banca y el asesoramiento entre las naciones europeas, las mismas que son blanco de las apuestas en contra que están sugiriendo.

El miércoles, Goldman y otros dos grandes bancos patrocinaron una presentación en Londres, en la que el secretario de Economía español, José Manuel Campos, planeaba esbozar las medidas de austeridad fiscal de España y presentar a los inversionistas el caso español, de acuerdo con una invitación vista por The Wall Street Journal. Goldman goza de una posición de liderazgo entre los bancos para facilitar la venta de deuda soberana española.

En el pasado, firmas de Wall Street han buscado vender a los fondos de cobertura (hedge funds) ideas que serían rentables en caso de descalabros. Antes de la crisis financiera de 2008, Goldman y otras firmas financieras sugirieron a sus clientes en los fondos de cobertura apuestas a la baja en el mercado inmobiliario que incluían los seguros contra la cesación de pagos —contratos que aumentan en precio si cae el valor del activo subyacente— creados por los bancos. En ocasiones, Goldman apostó a la caída de valores hipotecarios, mientras los vendía a otros clientes que apostaban a que subieran.

Sin embargo, las ideas de corretaje en el informe de Brazil son diferentes a los productos relacionados con hipotecas vendidos por Goldman, ya que estas sugerencias incluyen productos financieros existentes, tales como opciones e índices. Como «creador de mercado» en los productos enumerados en el informe de Brazil, Goldman ofrece ejecutar las operaciones que describe. Cuando Goldman maneja tales negociaciones, recibe comisiones más altas que cuando ejecuta operaciones bursátiles, cuyo rendimiento es apenas de algunos centavos por acción. Las propias posiciones de corretaje de Goldman podrían beneficiarse si los fondos de cobertura y otros clientes adelantan operaciones basados en el informe. Goldman destaca al comienzo del documento que otros operadores de la firma, o «personal de Goldman Sachs», ya podrían haber actuado a partir de lo que indica el informe.

Por supuesto, Brazil no es el único que tiene una visión sombría de Europa: el pesimismo sobre el continente abunda por estos días en Wall Street. Brazil tampoco tiene una fórmula infalible sobre los instrumentos financieros en el informe.

Una visión privilegiada

Por ejemplo, la unidad de Investigación de Economía Global, Commodities y Estrategia de Goldman publicó un informe de divisas extranjeras en julio que menciona las perspectivas de las puestas pesimistas contra el euro versus tanto el dólar como el franco suizo. Otros bancos de inversión tienen estrategas que también les brindan a fondos de cobertura ideas de corretaje.

El informe, divulgado por el grupo de Estrategias para fondos de cobertura de la división de valores de Goldman, brinda un vistazo de las ideas de corretaje que se generan para fondos de cobertura a través de estrategas, como Brazil, quienes son parte de la operación de corretaje de Goldman y no de su grupo de investigación.

Ese tipo de estrategas se sienta junto a los corredores que ejecutan las operaciones para sus clientes. A diferencia de los analistas en las divisiones de investigación de las firmas —que se supone que están aislados de la información sobre la actividad de los clientes de las firmas—, los escritorios de estos estrategas tienen una vista privilegiada para ver el descenso y el flujo de jugadas de inversión de los clientes.

Pueden ver si hay una ola de interés entre los fondos de cobertura para hacer apuestas pesimistas en un sector determinado, y observan si los volúmenes de corretaje se reducen o explotan. Su punto de vista está informado por más información, a menudo confidencial, sobre clientes que las opiniones de los analistas, por lo que su investigación e ideas se vuelven muy cotizadas entre los corredores.

El trabajo de Brazil incluye detalles acerca de los problemas de los mercados que en general no aparecen en una investigación para la difusión pública. Los fondos de cobertura deberían «prepararse para la tormenta», sugiere.

«Aquí vamos de nuevo», dice en el informe, en medio de una serie de gráficos que muestran las estadísticas negativas similares a las que presagiaban problemas antes del pánico financiero de 2008. «Resolver un problema de deuda con más deuda no ha resuelto el problema de fondo. En Estados Unidos, el crecimiento de la deuda del Tesoro financió al consumidor estadounidense, pero no ha tenido un impacto suficiente en el crecimiento del empleo. ¿Puede EE.UU. seguir depreciando la divisa base de todo el mundo?», se pregunta Brazil.

En el informe, el autor explica en detalle el nivel de endeudamiento de 77 instituciones financieras europeas, entre las que identifica algunas con alto nivel de apalancamiento. Tales detalles son valiosos para los inversionistas que buscan hacer apuestas bajistas a través de seguros contra la cesación de pagos de bancos europeos individuales, afirman gestores de fondos de cobertura.

Para los inversionistas que quieren hacer una apuesta más amplia contra las instituciones financieras europeas, Brazil sugiere comprar seguros contra la cesación de pagos a cinco años en un índice que refleja el crédito de una serie de empresas europeas. Alrededor de 20% de las que forman parte del índice, el «iTraxx Europe serie 9», son bancos y compañías de seguro, escribe el autor.

También sugiere una opción de venta a seis meses para dar a los inversionistas el derecho a apostar contra el euro frente al franco suizo. El euro «puede debilitarse si los paquetes adicionales de ayuda financiera o las medidas de estímulo reciben su aprobación por parte de los gobiernos europeos», señala.