La sucesión de fraudes, quiebras y crisis que han marcado las últimas décadas —desde esquemas Ponzi monumentales hasta quiebras tecnológicas y manipulación de índices de referencia— no es un punteo de anécdotas aisladas. Constituye, más bien, la señal de un fallo sistémico: la colisión entre incentivos privados mal alineados, arquitecturas regulatorias fragmentadas y una cultura pública que ha normalizado la incomprensión de los riesgos financieros. El resultado es un mercado que, con demasiada frecuencia, traslada pérdidas a familias, empleos y estabilidad social.

.

Casos paradigmáticos: síntesis y lecciones

Bernard Madoff representa la cara más dramática y humana del desastre. Sentenciado a la pena máxima —150 años de prisión— por montar lo que se considera el mayor esquema Ponzi conocido, su caso recordó que la enorme sofisticación aparente puede ocultar fragilidad operativa, y que la connivencia involuntaria o deliberada de intermediarios agrava la tragedia. La documentación judicial y las crónicas periodísticas conservan el relato de una estafa que arrasó el patrimonio de particulares, fundaciones y fondos.

Las investigaciones y demandas posteriores pusieron el foco sobre bancos que habían tratado con Madoff, y uno de los capítulos más ilustrativos fue el acuerdo de JPMorgan Chase: la entidad acordó en 2014 pagar 2.600 millones de dólares para resolver reclamaciones relacionadas con su presunta inacción pese a señales de alerta. Ese acuerdo no borra la pregunta central: ¿hasta qué punto las instituciones financieras toleraron o ignoraron irregularidades por interés propio?

El caso del fondo Abacus, con Goldman Sachs en el centro, mostró otro riesgo: el conflicto de agencia. En 2010 la Securities and Exchange Commission (SEC) resolvió una denuncia contra Goldman por la comercialización de un producto sintético ligado al mercado hipotecario, con un acuerdo por 550 millones de dólares y exigencias de reforma en prácticas comerciales. La acusación no era mera mala praxis técnica: señalaba que los diseñadores del producto tenían posiciones contrarias a las de los clientes a quienes se les vendía, una estructura que convierte al asesor en jugador y vendedor al mismo tiempo.

Más reciente en la cronología, Wirecard —la fintech alemana entonces alabada por mercados y gobiernos europeos— colapsó cuando se descubrió que cerca de 1.900 millones de euros «faltaban» en sus cuentas. La compañía entró en insolvencia y su caída puso en evidencia fallas de auditoría, supervisión y credulidad política. La lección es doble: las narrativas de éxito tecnológico pueden enmascarar déficits de control, y la presión política para preservar empleos o relato económico puede retardar controles efectivos.

En el nuevo terreno de las criptomonedas, el derrumbe de FTX es el ejemplo vivo de cómo modelos de negocio opacos y conflictos operativos pueden traducirse en pérdidas planetarias. La caída de FTX y el proceso penal contra su fundador muestran que la ausencia de reglas claras y supervisión efectiva en mercados emergentes produce víctimas masivas —clientes minoristas incluidos— y exige respuestas regulatorias contundentes. En 2024, la justicia estadounidense condenó y sancionó duramente a los responsables de esa trama.

Finalmente, la manipulación de índices referenciales (como la LIBOR) y la constatación de mercados de divisas concertados descubiertos por autoridades, han sido episodios que erosionaron la confianza en la infraestructura misma del mercado, con multas y procesos contra bancos globales. Estos hechos confirman que no basta con supervisores débiles o sanciones ex post: hay que modelar incentivos para evitar la captura y el abuso antes de que el daño sea sistémico.

A finales de 2022 y principios de 2023, los ejecutivos clave de FTX y Alameda, Caroline Ellison , Gary Wang y Nishad Singh, se declararon culpables de defraudar a clientes de FTX y cargos relacionados. Los tres declararon que fue Sam Bankman-Fried quien les ordenó cometer el fraude.

.

Causas estructurales: por qué se repiten las fallas

No existe una única explicación; hay un mosaico de factores que interactúan:

—Desalineación de incentivos: remuneraciones basadas en resultados de corto plazo, estructuras de comisiones y posiciones en sentido contrario fomentan la toma de riesgos oportunista.

—Complejidad opaca: productos financieros empaquetados en estructuras casi herméticas resultan ininteligibles para la mayoría de supervisores y clientes.

—Regulación fragmentada y política débil: la regulación frecuentemente es reactiva, capturada por intereses sectoriales o limitada por fronteras nacionales en un mercado que opera globalmente.

—Cultura institucional permisiva: cuando la reputación y el lobby institucional pesan tanto como la ley, la prudencia queda subordinada a la ganancia. Alan Greenspan, en su testimonio de 2008, reconoció una falla de juicio en confiar en que la autorregulación sería suficiente para contener excesos. Esa admisión pública resalta el problema: las creencias ideológicas pueden volverse riesgos sistémicos.

Paul Volcker, por su parte, sintetizó con ironía el descrédito de una «innovación» financiera que ha generado más complejidad que valor social, cuando observó que muchas de las llamadas innovaciones no habían contribuido al crecimiento real en la economía; su comentario sobre el cajero automático se ha transformado en emblema de una crítica mayor a la deriva de la ingeniería financiera

Qué funciona y qué no: principios de una reforma creíble

La prevención del próximo gran fraude exige medidas que combinen técnica, institucionalidad y cultura pública:

1. Órganos reguladores verdaderamente independientes. No basta con crear entidades; hay que blindar su financiación, rotación de personal y mecanismos contra la captura política. La autonomía debe ser real y operativa.

2. Transparencia operativa radical. Registros centralizados de posiciones, contrapartes y exposición a derivados que permitan auditorías en tiempo razonable y acceso razonado por autoridades.

3. Fiduciaria obligatoria y sanciones personales. Endurecer la responsabilidad legal de ejecutivos y auditores, con sanciones proporcionales y realistas que disuadan la toma de riesgos deliberada.

4. Herramientas de supervisión tecnológica. Reguladores con capacidades analíticas para detectar patrones anómalos (matching de transacciones, análisis de redes, control estadístico) antes de que las pérdidas se escalen.

5. Cooperación internacional. Los productos y flujos transfronterizos exigen marcos acordados y procedimientos de ejecución que no permitan a actores trasladar operaciones a jurisdicciones de baja vigilancia.

6. Protección y premio al whistleblower. Incentivos para empleados y consultores que detecten irregularidades y las eleven con garantías reales.

7. Educación financiera pública. Una ciudadanía que entienda los productos, y que pueda exigir mejores prácticas, constituye la defensa última contra la normalización de abusos.

Además, en mercados nuevos (fintech, criptomonedas) es imprescindible aplicar el principio de «prudencia antes que permisividad»: la innovación no puede ser un asidero para eludir supervisión. Los casos de las criptomonedas $LIBRA y Diem —una estafa pump & dump y un caso de vacíos normativos, respectivamente— alertan sobre la necesidad de marcos claros desde el diseño.

La educación financiera es clave para evitar los fraudes.

Entre la ética y el mercado: la necesidad de un capitalismo más humano

Frente a este escenario, la discusión va más allá de reformas puntuales. Lo que está en juego es el sentido mismo del sistema económico global. El Papa Benedicto XVI, en su encíclica Caritas in Veritate, subrayó que “la economía necesita de la ética para su correcto funcionamiento”. No se trata de moralizar superficialmente los mercados, sino de reconocer que, sin un anclaje en valores, las finanzas se convierten en un casino global que traslada las pérdidas a los más vulnerables.

El Distributismo, inspirado en la Doctrina Social de la Iglesia y defendido por pensadores como G.K. Chesterton y Hilaire Belloc, proponía desde principios del siglo XX un modelo donde la propiedad y la producción estuvieran más equitativamente distribuidas. Aunque en gran medida fue relegado por la hegemonía del capitalismo financiero, existen ejemplos de empresarios que buscaron ese equilibrio. En Argentina, Enrique Shaw —hoy en proceso de beatificación— mostró que era posible conjugar rentabilidad económica con respeto a la dignidad humana, uniendo eficiencia empresarial con compromiso social.

Enrique Ernesto Shaw (1921-1962) fue un empresario católico argentino. Por su vida ejemplar, la Iglesia inició su proceso de canonización. Fue director general de Cristalerías Rigolleau, donde puso en práctica con muy buenos resultados los principios económicos de la Doctrina Social de la Iglesia. Fundó la Asociación Cristiana de Dirigentes de Empresa (ACDE).

.

La resistencia a la regulación

Cada intento de imponer controles más estrictos a las instituciones financieras se topa con la resistencia férrea de lobbies y parlamentos. La reforma de Wall Street posterior a 2008, conocida como Dodd-Frank, fue denunciada por Madoff como un chiste. Y, en efecto, buena parte de sus disposiciones fueron luego diluidas. La lógica de los ciclos electorales, sumada a la influencia del dinero en la política, hace que la reforma estructural del sistema financiero sea siempre una promesa postergada.

Es sabido que la acumulación de capital en muy pocas manos tiende a crear desigualdades extremas si no se establecen mecanismos correctivos. El problema es que esas desigualdades no son solo económicas: generan un poder político que captura al Estado, impidiendo que las regulaciones se materialicen.

No todos los problemas se resuelven con normas técnicas. La restauración de la confianza requiere un cambio cultural: una ética pública que presuma responsabilidad en la esfera financiera y una dirigencia dispuesta a sacrificar ventajas de corto plazo por la estabilidad y el bien común. La justicia, entendida como sanción ejemplar y reparación real a las víctimas, tiene un componente simbólico importante; pero sin reformas estructuradas la sanción individual se queda en anécdota.

Las sanciones monumentales y las condenas dramáticas generan titulares, pero sin arquitecturas que impidan la repetición del delito, el mercado permanecerá vulnerable. En otras palabras: la justicia punitiva sin arquitectura preventiva es meramente paliativa.

Entrar en acción

El diagnóstico está claro: cuando la búsqueda del rendimiento convierte al mercado en un laberinto opaco y sus actores en agentes que entran en conflicto con los intereses de sus clientes y del público, la receta para la catástrofe está servida. Evitar el próximo carnaval financiero exige, simultáneamente, fortalecimiento institucional, translación de incentivos y una renovación ética del ejercicio profesional en finanzas.

Propongo tres pasos operativos y urgentes: (1) blindar la independencia y la capacidad técnica de los reguladores; (2) imponer requisitos de transparencia operativa en tiempo real para instrumentos complejos; (3) endurecer la responsabilidad fiduciaria con sanciones efectivas contra directores, auditores y gestores que oculten o faciliten fraudes. Si la economía no pone límites al oportunismo interno, la próxima crisis no será un fallo técnico: será la consecuencia previsible de decisiones humanas.

El mercado financiero no es una ruleta ni un teatro para ganancias sin costo colectivo. Es una infraestructura social que funciona —o falla— según las reglas que la sociedad impone. La tarea es política y técnica, requiere voluntad ciudadana y decisión de la dirigencia. Actuar ahora no es un ademán moral: es una inversión en estabilidad, crecimiento y en la dignidad de millones que confían sus ahorros, pensiones y esperanzas a instituciones que deben responder por ellas.

Un panel de arbitraje de tres personas supervisado por Finra Dispute Resolution Services sorprendió a la industria de asesoramiento financiero el miércoles 12/03/25 y otorgó a los clientes de Stifel Financial Corp. U$S 132,5 millones en daños y honorarios legales en una disputa centrada en un corredor estrella de Stifel en Miami, Chuck Roberts .

.

En 2023, David Jannetti y sus familiares demandaron a Stifel Nicolaus & Co., la subsidiaria de corretaje de Stifel Financial, reclamando al menos 5 millones de dólares en daños relacionados con inversiones en Notas estructuradas, una estrategia que ha dado lugar a varias reclamaciones de arbitraje importantes previas y daños a los clientes.

Pero la decisión de arbitraje del miércoles, dictada por un panel de FINRA en Boca Ratón, Florida, es la más significativa. «Este es el mayor laudo arbitral en el sector minorista en la historia de la FINRA», declaró Jeff Erez, abogado de la familia Jannetti y de otros inversores que han demandado a Stifel por daños y perjuicios relacionados con Notas estructuradas. Erez señaló que solo los inversores institucionales han obtenido mayores victorias en cuanto a los daños que las empresas han tenido que pagar a sus clientes.

Financial Industry Regulatory Authority, Inc es una corporación privada regulatoria estadounidense encargada de gobernar y gestionar la actividad entre corredores de bolsa, consultores y el público inversionista.

.

“El panel de arbitraje realmente le dio una paliza a Stifel”, dijo Andrew Stoltmann, abogado del demandante. “Esto es una gran y vergonzosa mancha de sangre”.

Según el último informe de resultados de Stifel Financial, de enero, la compañía generó en 2024 la suma de 2.420 millones de dólares en ingresos antes de impuestos gracias a su grupo global de Gestión patrimonial. El laudo arbitral del miércoles representa cerca del 5,4 % de los ingresos de Stifel por gestión patrimonial del año pasado.

.

Stifel ha perdido previamente demandas derivadas de la venta de Notas estructuradas por parte de Roberts. En noviembre, un panel de arbitraje de FINRA otorgó a los inversores 2,35 millones de dólares en una demanda; un mes antes, otro grupo de árbitros otorgó a los inversores 14,2 millones de dólares en una demanda similar, incluyendo 9 millones de dólares en daños punitivos.

“Estos son casos sólidos y los mensajes de texto son una gran razón por la que los clientes los ganan”, dijo Erez. “Hay 16 demandas más por venir”.

En el laudo de esta semana, los árbitros ordenaron a Stifel Nicolaus pagar a David Jannetti y a su familia 26,5 millones de dólares en daños compensatorios, 79,5 millones de dólares en daños punitivos y 26,5 millones de dólares en honorarios y costas legales. Las indemnizaciones por daños punitivos son poco frecuentes en los arbitrajes de la FINRA.

El asesor de Stifel en el centro de la disputa, Chuck Roberts de Miami Beach, no fue demandado en el asunto, pero fue mencionado cuatro veces en el laudo de Finra.

“Stifel planea solicitar la revisión judicial de esta indemnización desorbitada, que no se sustenta ni en los hechos ni en la ley”, declaró la compañía en un comunicado de prensa el jueves por la mañana. “Las demandas fueron presentadas por una familia sofisticada de inversores experimentados y agresivos que comprendieron los riesgos, participaron en la selección de inversiones, las supervisaron de cerca y solo presentaron quejas tras sufrir pérdidas”.

El panel de arbitraje de FINRA señaló la “conducta atroz” de Stifel en el asunto, según el documento del laudo.

Stifel “tenía conocimiento real de la ilicitud de la conducta y de la alta probabilidad de que se causaran lesiones o daños a los demandantes y, a pesar de ese conocimiento, persiguió intencionalmente ese curso de conducta, lo que resultó en daños”, según el laudo.

Esa conducta de Stifel incluyó: concentrar excesivamente las cuentas de los clientes en Notas estructuradas, así como en industrias limitadas; ignorar la filosofía de inversión de los clientes; y colocar los intereses financieros de Stifel por delante de los intereses de los clientes. [En pocas palabras ignorar lo prescripto por la Norma ISO 22222. Nota de EP]

Stifel también permitió y promovió productos de Notas estructuradas personalizadas mediante mensajes de texto, lo que infringía los requisitos de registro de la Comisión de Bolsa y Valores (SEC), ya que dichos mensajes contenían terminología inexacta y engañosa, según el laudo. Sin embargo, dichos mensajes de texto no se incluyeron en la decisión del panel de FINRA.

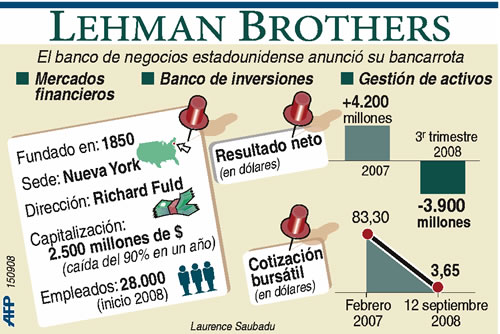

Lehman Brothers Holdings Inc, fundada en 1850, fue una compañía global de servicios financieros de Estados Unidos. Destacaba en banca de inversión, gestión de activos financieros e inversiones en renta fija, banca comercial, gestión de inversiones y servicios bancarios en general.

Lehman Brothers sobrevivió a una guerra civil, a la crisis bancaria de 1907, similar a la originada en 2008, a la crisis económica mundial conocida como el crac de 1929, a escándalos en su papel de intermediador de bonos y a colapsos en hedge funds, pero no consiguió superar la crisis subprime de 2008 que constituye, con un pasivo de $613.000 millones, la mayor quiebra de la historia hasta el momento. El 15 de septiembre de 2008, Lehman Brothers anunció la presentación de su quiebra. Fuente: Wikipedia, 2016.

Las personas clave de un banco de inversión, 24 horas antes de la crisis subprime, están tratando de deshacerse de los bonos hipotecarios malos presentándolos como una inversión segura y rentable a sus clientes.

.

Inspirada en el colapso de Lehman Brothers y el escándalo de las hipotecas subprime que marcó el inicio de la crisis financiera global de 2008.

Investors considering stocks have a din of data to sift through today.

Unfortunately, quantity is no guarantee of quality: It has never been harder for small investors to assess which information they should rely upon to make decisions. As a result, some investors have depended too heavily on the one-word recommendations of just a few analysts—without understanding the particular context in which such recommendations often are generated, and the particular ways in which they often must be read.

Analysts play a useful role in our capital markets. For example, by doing in-depth research for their large institutional clients and employers, analysts can help substantial sums of capital be directed to more productive uses in our economy.

This article explains what analysts do and places it in perspective, so investors can learn what other information they need for managing their portfolios.

The two key takeaways are: 1) analysts’ ratings do not have clear, standardized meanings; and 2) analysts might have potential conflicts of interest that you, as an investor, should be aware of in assessing the usefulness to you of any particular analyst recommendation.

Same Word, Different Meanings

Analysts usually summarize their research reports with a brief recommendation. Every firm uses its own rating system. Here are examples from three firms:

Firm A

Firm B

Firm C

Buy

Strong Buy

Recommended List

Outperform

Buy

Trading Buy

Neutral

Hold

Market Outperformer

Underperform

Sell

Market Perform

Avoid

Market Underperformer

As you can see, comparing these ratings scales is not easy. The same term might mean one thing for one firm and something else for another firm:

For example, as you can see above, Firm A rates its most positive recommendations as «Buy,» but Firm B does not. When Firm B uses a «Buy,» it means that Firm B likes the stock, but not as much as the stocks that it rates «Strong Buy.»

Likewise, one firm’s «Underperform» might mean that it expects a stock to appreciate 10 percent slower than the overall market over an 18-month period. For another firm, the same term «Underperform» might mean that it expects the stock to drop 5 percent within a 12-month period.

Clear «Sell» ratings have grown rare. Some firms no longer even use «Sell» or any word obviously like it. Frequently, a «Hold» rating in effect means «Sell.»

Even providers of so-called «consensus» ratings, such as I/B/E/S and First Call, use their own rating scales. These organizations apply numerical formulas to map several analysts’ different ratings scales to their own rating conventions. They then average their standardized recommendations to create a «consensus» rating for a particular security.

For all these reasons, it can be potentially damaging to your portfolio to automatically accept an analyst recommendation. Before you act on a recommendation, keep the following in mind:

Is it right for YOU? A «Buy» rating does not mean that every investor should acquire the stock. Nor does a «Sell» rating mean that every investor should immediately sell it. Your own financial situation and investment needs are what matter. If you consider any individual rating, do not view it in absolute or abstract terms, but in the context of your own unique financial situation.

Never rely on a rating alone. Do your investment homework. When considering an analyst recommendation, look at the full research report, not just the one-word rating. The full report will often provide information that is essential to explain risk factors or to put the recommendation into its proper perspective.

Analysts differ in quality. As in any other field, not every analyst can be the best. To learn about different analysts’ track records, you can either follow their recommendations over time, or refer to rankings that are found in certain investor-oriented magazines, newsletters and Internet websites. Some websites provide consensus recommendations, essentially an average of a number of analysts’ recommendations.

Conflicts of Interest

Research analysts study companies and draw on a wealth of industry, economic, and business trend information to help their clients make better investment decisions. Retail investors may believe that most analysts’ primary obligation is to the investing public. In fact, the full story is much more complicated.

Some analysts are unaffiliated: they sell their independent research to financial or investing institutions, banks, insurance companies or private investors on a project or subscription basis. But a large number of analysts are employed by institutions whose financial stake in their recommendations may go well beyond their accuracy.

For example, many analysts work for large financial firms that underwrite securities. An underwriter acts as an intermediary between the company publicly offering securities and investors buying the new stock. Even after the initial public offering, or IPO, it may have an ongoing relationship with the company or own a significant amount of the company’s stock. And it will often stand to benefit from analyst recommendations that would tend to support the price of, or encourage trading in, that security.

Other analysts work for institutional money managers, such as mutual funds, hedge funds or investment advisers. They may provide research and advice for institutional clients whose investment decisions can differ significantly from those faced by ordinary investors. A mutual fund that relied on its analyst’s earlier positive recommendation in acquiring the stock of a company might be harmed by any revised recommendation that would tend to lower the market value of the security.

Just by thinking about these kinds of employment arrangements, you can begin to imagine the kinds of conflicts that analysts may face as they develop and offer their opinions in research reports. For example:

Investment Banking Relationships. Providing investment banking services, such as underwriting an IPO or advising on a merger or acquisition, can be a lucrative source of revenue for an analyst’s firm. Thus, the analyst may feel an incentive not to say or write things that could jeopardize existing or potential client relationships for their investment banking colleagues. On the other hand, the analyst may also be more knowledgeable or diligent in his research because his firm did the underwriting.

Analyst Compensation.Brokerage firms’ compensation arrangements can put pressure on analysts to issue positive research reports and recommendations. For example, many analysts are paid at least partly and indirectly on the basis of their firms’ underwriting profits. So they may be reluctant to make recommendations that could reduce such profits, and hence their own compensation.

Brokerage Commissions. An analyst’s report can help firms make money indirectly by generating more buying and selling of covered securities—which, in turn, result in additional commissions for the firm.

Buy-Side Pressures.A mutual fund with large holdings in a stock has little desire to see an analyst put out a «Sell» recommendation on that security and possibly contribute to a sharp decline in its price. Hence the proliferation of euphemistic ratings—such as «Hold,» «Retain,» and «Market Perform»—which small investors may take at face value, but which professional and institutional investors know are often tantamount to «Sell.» As a result, ratings inflation became as widespread and unhealthy in our markets as grade inflation in our schools.

Ownership Interests in the Company. An analyst, other employees, and the firm itself may own significant positions in the companies or market sectors on which the analyst conducts research and makes recommendations. The analyst may own such shares directly, or through employee stock-purchase pools.

These economic realities certainly do not mean that analysts are corrupt or even biased. But because analysts are called upon to make so many judgments that are not black and white, any of the above factors can put pressure on their objectivity—no matter how honest or competent they may be. So you should bear these realities in mind before making an investment decision.

Making Your Investment Decision

The fact that analysts or their firms may have conflicts of interest does not mean that their recommendations are without value. Often research reports will contain quantifiable measures—such as earnings predictions or comparisons to other companies in an industry sector—that you may decide provide useful insight even if you do not take the analyst’s rating at face value. In any case, you should take all potential conflicts into consideration in assessing how much weight you should give the recommendation.

The important thing to remember is that you should never rely solely on an analyst recommendation when making an investment decision. There are many other important sources of information and factors you may wish to consider. For example:

Research the company’s reports yourself, using the SEC’s EDGAR database. If you do not have access to the Internet, call the company for copies. If you can’t analyze them on your own, ask your broker or another trusted financial professional for help.

Speak with your broker or financial adviser and ask questions about the company and its prospects. When doing so, ask your broker about the relationship of his own firm, if any, to the company whose stock you are considering.

Learn about the company by consulting independent news reports, commercial databases, and other references.

Find out whether the analyst’s firm underwrote one of the company’s recent stock offerings—especially its initial public offering (IPO).

Find out more about analyst recommendations by consulting your broker or some of the other sources discussed in this Guide.

In short, whatever a given analyst recommendation may say, always consider whether a particular investment is right for you in light of your own financial circumstances. Remember, you are the boss, it’s your money, and your situation and goals that matter.

NBER Working Paper No. 11728 Issued in November 2005 NBER Program(s): CFIFM

Developments in the financial sector have led to an expansion in its ability to spread risks. The increase in the risk bearing capacity of economies, as well as in actual risk taking, has led to a range of financial transactions that hitherto were not possible, and has created much greater access to finance for firms and households. On net, this has made the world much better off. Concurrently, however, we have also seen the emergence of a whole range of intermediaries, whose size and appetite for risk may expand over the cycle. Not only can these intermediaries accentuate real fluctuations, they can also leave themselves exposed to certain small probability risks that their own collective behavior makes more likely. As a result, under some conditions, economies may be more exposed to financial-sector-induced turmoil than in the past. The paper discusses the implications for monetary policy and prudential supervision. In particular, it suggests market-friendly policies that would reduce the incentive of intermediary managers to take excessive risk.

S&P acuerda pagar una multa de US$1.500 millones para resolver un litigio en EE.UU.

Por Timothy W. Martin.

NUEVA YORK (EFE Dow Jones) — Standard & Poor’s Ratings Services acordó el martes pagar una multa de US$1.500 millones para resolver un litigio por supuestamente otorgar calificaciones elevadas a activos hipotecarios antes de la crisis financiera 2008.

La agencia calificadora pagará US$687,5 millones al Departamento de Justicia estadounidense, y otro importe similar a 19 estados y al Distrito de Columbia. La agencia alcanzó un acuerdo separado por el que pagará US$125 millones al Fondo de Pensiones de los Funcionarios de California.

El gobierno acusó a S&P de deliberadamente engañar a los inversionistas al otorgar calificaciones triple A a activos hipotecarios. Estas valoraciones resultaron ser incorrectas con el desplome del mercado inmobiliario, y provocaron rebajas generalizadas de calificaciones y contribuyeron a provocar la crisis financiera.

S&P no ha reconocido que llevara a cabo malas prácticas como parte del acuerdo, y afirma que no hay pruebas de que violara ninguna ley.

Este acuerdo resuelve una demanda interpuesta por el Departamento de Justicia estadounidense y algunos estados en 2013, y supone la multa más alta jamás pagada por una agencia de ratings para resolver un caso de uso de calificaciones elevadas antes de la crisis.

The Financial Industry Regulatory Authority is examining how major investment banks and brokerage firms define and manage conflicts of interest between themselves and their clients. Will the first systematic look at conflicts on Wall Street in years make a difference for investors?

Enlarge Image

In the next few weeks, according to Susan Axelrod, an executive vice president at Finra, its regulators will start to examine 14 big firms, which she declined to name.

Finra—a self-regulatory organization funded by the securities industry—telegraphed its intentions in May, when its chief executive, Richard Ketchum, said in a speech that «we will look to have a focused conversation with you about the conflicts you have identified and the steps you have taken to eliminate, mitigate or disclose each of them.»

Mr. Ketchum added that he would like detailed reviews of conflicts of interest to «become a standard part of operating procedure» on Wall Street.

Finra’s call appears to be the first time in nearly a decade that regulators have explicitly targeted the question of how Wall Street handles conflicts of interest. In a speech in 2003, Stephen Cutler, then director of enforcement at the Securities and Exchange Commission (and now general counsel of J.P. Morgan Chase JPM +0.56% ), urged every financial firm to run a «top-to-bottom review» that would seek to correct «conflicts of interest of every kind.» He added, «No one is in a better position than you to identify» such conflicts.

Mr. Cutler’s speech, say other regulators, led to an outpouring of submissions to the SEC in which firms laid out the conflicts they had identified and the safeguards they had put in place to control them.

Investors should bear two things in mind in light of Finra’s examinations.

First, conflicts of interest aren’t a part of how Wall Street does business; conflicts are its stock-in-trade. Even as they were professing their purity to the SEC in response to Mr. Cutler’s call, many firms turned out to be enticing ignorant borrowers into taking out mortgages they couldn’t afford, unloading portfolios of toxic debt on unsuspecting clients and manipulating one of the world’s most widely used interest rates for their own benefit.

«We understand that conflicts exist,» says Ms. Axelrod of Finra. «What defines firms and their culture is how they deal with those conflicts.»

Even so, it might be too much to expect Wall Streeters to identify their own conflicts.

In a recently published study, researchers led by behavioral economist George Loewenstein of Carnegie Mellon University asked hundreds of physicians and financial planners to evaluate conflict-of-interest policies. Half of each group read a set of proposed rules to minimize conflicts for doctors; the other half saw almost-identically worded rules to reduce conflicts for financial planners.

The doctors were outraged that financial advisers might accept pens, coffee mugs, free meals or educational junkets from investment companies. Yet the physicians rejected the idea that accepting pens, coffee mugs, free meals or educational junkets from drug companies could ever compromise the integrity of doctors.

The financial planners wanted doctors to be barred from accepting gifts from pharmaceutical companies, lest their objectivity be compromised—but thought the same restrictions in their own profession would be unnecessary and onerous.

In short, our eagle eye for spotting other people’s biases is blind as a bat’s to our own.

«Each of us tends to think that we are much more fair and more impartial than other people are,» says Prof. Loewenstein. «So we believe there’s no need for us to worry that we might be influenced by conflicts of interest, even as we think everyone else is.»

«There’s plenty of people who sell bad stuff knowingly,» says Robert Seawright, chief investment officer at Madison Avenue Securities, a financial-advisory firm in San Diego, «but I think the far bigger problem is inappropriate sales that are well-intended. I’ve seen people who sell bad stuff to their moms, because they thought it was the right thing.»

Remember now, as always, that the individual investor is at the bottom of Wall Street’s food chain—a speck of plankton adrift in a sea of predators.

The challenge is to defend yourself without being offensive. Never forget to ask your financial adviser: What benefit is there for you in selling this investment to me? And with a kind voice and a smile, ask for the answer in writing.

Fuente: The Wall Street Journal, 2012.

{kind=link}