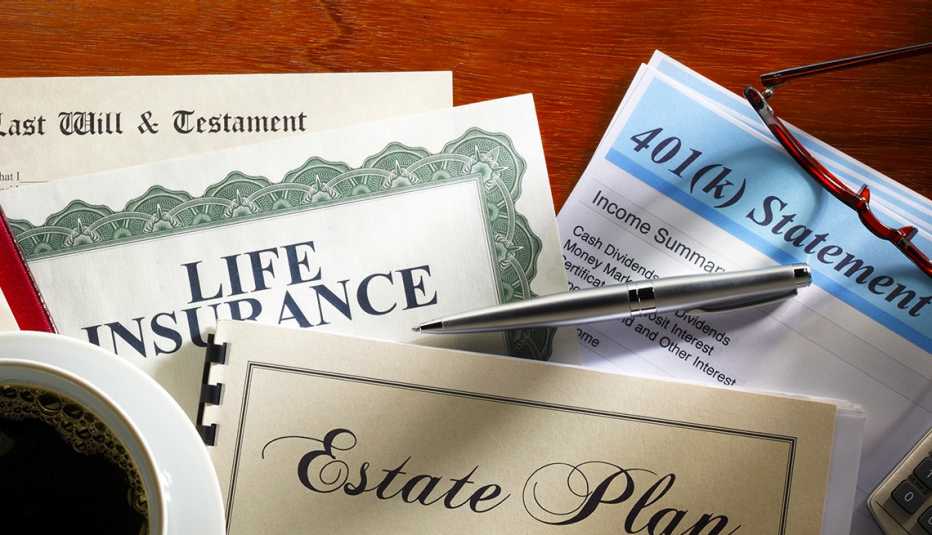

El mercado de seguros de vida enfrenta un desafío persistente: la falta de comprensión y percepción de necesidad por parte de los consumidores. Para agentes y brokers, aumentar el potencial de ventas requiere más que solo información; exige un enfoque estratégico basado en la ciencia del comportamiento, la comunicación efectiva y la tecnología. Como dijo Henry Ford: «Reunirse es un comienzo, permanecer juntos es un progreso y trabajar juntos es el éxito». Aplicar esta filosofía a la venta de seguros puede marcar la diferencia entre la inercia y el crecimiento sostenido.

El asesor financiero debe aplicar la metodología de Ventas Consultivas para alcanzar el éxito.

.

1. Desmitificar el Seguro de Vida: La clave de la Comunicación

El seguro de vida sigue siendo un producto financiero mal comprendido. La mayoría de los consumidores perciben su costo como prohibitivo y su utilidad como lejana. Según un estudio de LIMRA y Life Happens de 2024, el 73% de las personas sobreestima el precio de una póliza de seguro de vida y no sabe cómo encarar el proceso de compra de una póliza.

𝔸𝕔𝕔𝕚𝕠𝕟𝕖𝕤 𝕔𝕝𝕒𝕧𝕖:

– Presentar cifras reales y comparaciones accesibles para desmentir la percepción de alto costo.

– Explicar los beneficios en vida, como la acumulación de valor en efectivo y los beneficios por enfermedad terminal.

– Utilizar narrativas que conecten emocionalmente con los clientes, demostrando cómo el seguro de vida promueve el bienestar financiero de sus familias.

.

2. Personalización y Relevancia: Hablar el idioma del cliente

El consumidor actual espera experiencias personalizadas. La hiperpersonalización, basada en datos y comportamiento del usuario, permite ofrecer soluciones alineadas con sus necesidades y prioridades.

𝔼𝕤𝕥𝕣𝕒𝕥𝕖𝕘𝕚𝕒𝕤 𝕖𝕗𝕖𝕔𝕥𝕚𝕧𝕒𝕤:

– Utilizar herramientas de IA para segmentar clientes y ofrecer cotizaciones adaptadas a su perfil financiero.

– Implementar procesos de asesoría guiada, enfocándose en objetivos individuales, como planificación patrimonial o seguridad para la jubilación.

– Aprovechar momentos clave en la vida del cliente (matrimonio, nacimiento de hijos, compra de vivienda) para ofrecer soluciones adecuadas.

3. Ciencias del Comportamiento: Facilitando la Toma de Decisiones

Daniel Kahneman, en su libro Pensar rápido, pensar despacio, distingue entre pensamiento rápido e intuitivo y pensamiento lento y reflexivo. En el contexto del seguro de vida, las estrategias deben activar ambos procesos para generar decisiones informadas.

𝔸𝕡𝕝𝕚𝕔𝕒𝕔𝕚𝕠𝕟𝕖𝕤 𝕡𝕣𝕒́𝕔𝕥𝕚𝕔𝕒𝕤:

– Simplificar la presentación de información, resaltando los puntos clave con elementos visuales claros.

– Crear urgencia mediante estrategias como la escasez («beneficios especiales por tiempo limitado») y la prueba social («miles de familias ya han asegurado su futuro»).

– Incorporar testimonios de clientes satisfechos para generar confianza y credibilidad.

4. La Tecnología como aliada en la conversión

El mundo digital es un canal imprescindible para captar clientes. Con el 82% del tráfico de internet consumido en video, las estrategias digitales deben incorporar formatos audiovisuales.

ℍ𝕖𝕣𝕣𝕒𝕞𝕚𝕖𝕟𝕥𝕒𝕤 𝕚𝕟𝕕𝕚𝕤𝕡𝕖𝕟𝕤𝕒𝕓𝕝𝕖𝕤:

– Uso de redes sociales y contenido en video corto (Reels, TikTok, YouTube Shorts, X) para educar y atraer prospectos. Como ejemplo en nuestra Cuenta de X @GustavoIPadilla (con 20.000 seguidores) implementamos exitosas campañas de educación financiera y promoción del seguro de vida, con altas tasas de conversión.

– Implementación de chatbots y asistentes virtuales para responder consultas y guiar el proceso de compra.

– Aplicación de plataformas interactivas que permitan simulaciones de costos y beneficios en tiempo real.

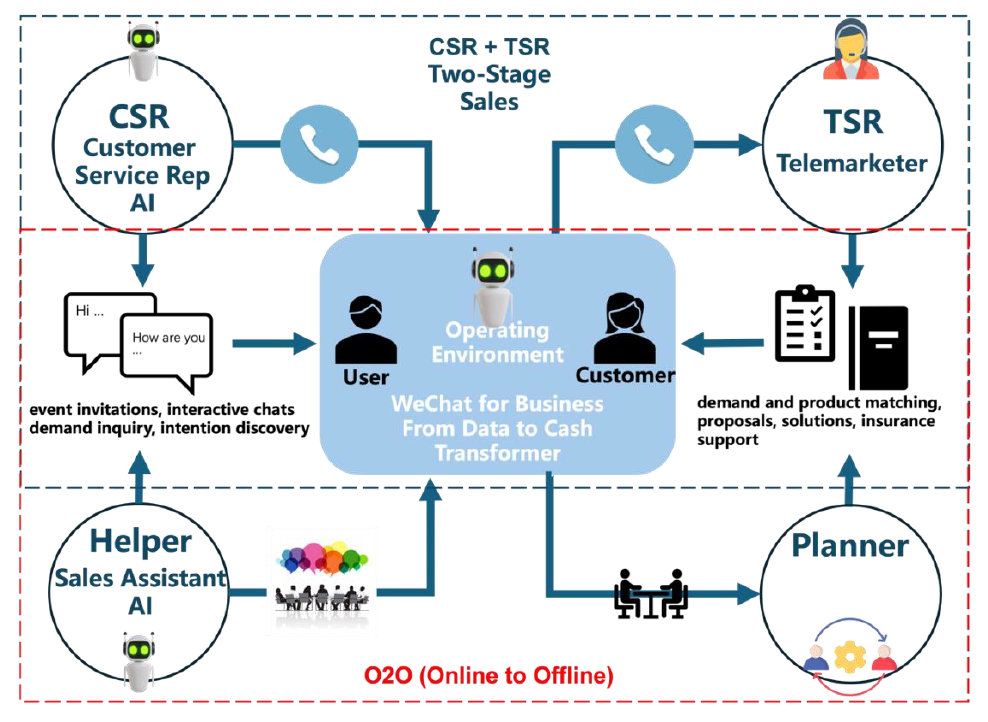

Esquema de una operación inteligente con apoyo de IA, en un modelo de marketing y ventas en dos etapas e integración de en línea a fuera de línea.

.

5. La Importancia del Factor Humano

Si bien la IA y la automatización potencian la eficiencia, la confianza en la compra de un seguro de vida sigue dependiendo de la interacción humana. Nada reemplaza la empatía y la asesoría de un agente experimentado. Además, al aumentar la oferta de contenido automatizado toma más relevancia el aporte de una Agente de carne y hueso.

𝔹𝕦𝕖𝕟𝕒𝕤 𝕡𝕣𝕒́𝕔𝕥𝕚𝕔𝕒𝕤:

– Potenciar la formación en Ventas Consultivas para entender y atender mejor las necesidades del cliente.

– Priorizar la construcción de relaciones a largo plazo en lugar de cerrar ventas rápidas.

– Implementar un seguimiento proactivo para acompañar a los clientes en cada etapa de su vida.

– Realizar docencia entre los potenciales clientes facilitando la comprensión de las finanzas personales. Aquí resulta muy valioso el aporte de nuestro Manual de Economía Personal. Cómo potenciar sus ingresos e inversionescomo herramienta para fomentar la Educación Financiera. Los estudios periódicos de LIMRA muestran la eficacia de esta estrategia.

-Combinar los enormes avances de la tecnología IA con las bases de la vieja escuela de próceres como José Salas Subirat, Napoleon Hill, Clement Stone o Brian Tracy.

La formación continua es clave para los consultores financieros.

.

La Venta de Seguros de Vida y Anualidades como una Misión

Incrementar la venta de seguros de vida y annuities no es solo una cuestión de estrategias de marketing, sino de educación, empatía y tecnología aplicada. Como afirmó Zig Ziglar: «Ayuda a suficientes personas a conseguir lo que quieren y tú conseguirás lo que quieres». Convertirse en un asesor de confianza, en lugar de solo un vendedor, es la clave para un crecimiento sostenible.

La oportunidad está en tus manos. Empieza hoy a transformar tu enfoque de ventas y construye un futuro más seguro y próspero para tus clientes y para tu negocio.

¿Cómo Planificar sus Finanzas Personales? ¿Cómo proteger sus ahorros? ¿Qué opciones tiene a su alcance? Acceso Libre y Gratuito, con inscripción previa. Versión grabada, usted accede en el horario que le quede más cómodo. Este seminario online gratuito le permitirá ingresar facilmente al Mundo Financiero Internacional y conocer los enormes beneficios de invertir con seguridad. Cientos de participantes ya conocen y disfrutan de estas ventajas y beneficios, ¡participe usted también! El webinario es gratuito y se realiza a través de nuestra de Sala de Conferencias virtual. Participe gratuitamente en un seminario onlinede una hora de duración y además reciba valiosos obsequios: un e-Book tituladoPor Qué Invertir en Wall Street, material adicional en formato digital y otros beneficios. ¡Todo esto en forma gratuita y sin compromiso!

BONO ESPECIAL: Quienes asistan a la reunión personal de Diagnóstico Financiero -sin cargo-recibirán como obsequio un ejemplar (en papel) del libro Manual de Economía Personal (168 págs.) Atención: Este Bono es por tiempo y stock limitado, ¡inscríbase ya! Promoción por tiempo limitado.

Seminario on line Cómo iniciar un Plan de Inversión Eficaz

Temario: • La planificación financiera. • El rol del consultor. • Objetivos, necesidades y recursos. • El horizonte temporal. • El riesgo. • La jurisdicción. • La moneda. • Los instrumentos de inversión. • La cartera de inversión. • La protección financiera. • La planificación sucesoria.

“Ninguna otra inversión financiera puede hacer lo que hacen las compañías de seguro de vida. Ninguna otra industria respalda sus productos con reservas tan saneadas como las de la industria del Seguro de Vida. Un ejemplo concreto es el de la Gran Depresión de 1929: cuando la Bolsa de New York tocó fondo y muchos bancos quebraron, las compañías de seguros pudieron dar a sus asegurados una seguridad que no pudieron encontrar en otro lugar. Otras industrias quebraron, se perdieron fortunas de un día para el otro, se evaporó el ingreso de las propiedades y los bienes raíces. Pero no se conoció ninguna pérdida por el fracaso de alguna compañía de seguros de vida. Ningún asegurado perdió un centavo. El récord de fuerza y seguridad de las compañías de seguros de vida, aún bajo las condiciones más adversas, es un emblema de orgullo en la industria del seguro. Ninguna inversión u otro tipo de negocio, ha tenido un récord de seguridad superior al del seguro de vida” Life Underwriter Training Council

Coronavirus: qué hacen los grandes inversores de Wall Street para sacar ventajas de la crisis del covid-19

Con Wall Street en caída libre, el precio del petróleo por los suelos, una posible recesión global y cada día más gobiernos cerrando fronteras o pidiéndoles a sus ciudadanos que se queden en la casa, el panorama económico parece desolador.

Entre las acciones que más se han desplomado están las de aerolíneas, cruceros y todo el sector turístico, además de los títulos del sector energético.

En medio de una guerra de precios petrolera, el barril de crudo cayó esta semana casi 10%, llegando a mínimos cercanos a u$s20 para el petróleo WTI que se transa en EE.UU. y el Brent, que se utiliza como referencia para los mercados europeos.

Entonces… si el petróleo está tan barato, ¿quién está comprando esas acciones?

Carl Icahn, el conocido inversor multimillonario estadounidense es uno de ellos. Al menos eso es lo que dijo en la prensa estadounidense, apuntando que ha comprado acciones de Occidental Petroleum.

«Ahora se ha llegado al punto en que algunas compañías están regaladas», le dijo Icahn a la cadena de noticias CNBC.

«Algunas de estas empresas son extremadamente baratas», señaló, agregando que las bolsas «probablemente tienen un largo camino para seguir cayendo».

Aunque la otra cara de la moneda, advirtió el multimillonario, es que existen compañías que están muy caras y con demasiada deuda, razón por la cual «deberían venderse».

Hay que decir que Icahn posee casi el 10% de Occidental Petroleum y que las acciones de esta firma han bajado cerca de 70% este año.

Otros títulos que el magnate dice haber comprado son Hertz y Hewlett-Packard.

Icahn pertenece al grupo de inversores que les gusta correr riesgos y que buscan el máximo beneficio cuando las bolsas están en crisis, conocidos informalmente en la jerga bursátil como «los especuladores» o «los oportunistas».

«Hay una división muy clara entre los inversores que piensan que es el momento de entrar al mercado y los que piensan que el derrumbe va a ser mayor», le dice a BBC Mundo Manuel Romera, profesor de finanzas de la IE Business School, España.

«Estamos en un momento muy delicado porque no ha aparecido dinero para comprar. La gente cree que esto es el apocalipsis», agrega.

Romera explica que la probabilidad de rentabilidad a futuro es elevadísima, pero «muchos de los que manejan fortunas creen que el suelo está más abajo».

El problema de estas crisis es saber cuál es la viabilidad financiera de una empresa para sobrevivir, explica.

«Algunos están invirtiendo en petróleo porque habrá compañías que subirán espectacularmente, pero habrá otras que van a quebrar», apunta el académico.

Rick Rieder, director gerente y jefe global de inversiones de BlackRock -el administrador de fondos más grande del mundo- advirtió que es probable que el mercado no haya tocando fondo.

«Hoy en día, me gustan las hipotecas y las acciones muy selectivas», apuntó Rieder.

«Estamos seleccionando algunas acciones que tienen un valor real en la atención de salud, tecnología y construcción».

Incluso si las empresas reciben un golpe en sus ganancias, agregó, «esta es una oportunidad única en la vida para obtener este tipo de activos».

El modelo Warren Buffet

«Hay que ser codicioso cuando los demás son miedosos y miedoso cuando los demás tienen los ojos inyectados de codicia».

Esa es una de las frases más conocidas del magnate estadounidense Warren Buffet, a quien le gusta ir contra la corriente, pero haciendo inversiones seguras.

Los ricos españoles abandonan Panamá y escapan a un nuevo paraíso fiscal: Estados Unidos

Despachos de abogados reciben órdenes de trasladar cuentas a Estados Unidos, que ofrece mayor privacidad que Suiza, Luxemburgo y las Caimán.

Estados Unidos está acogiendo en todo su territorio y en algunos de sus paraísos fiscales (por ejemplo los estados de Nevada, Wyoming y Dakota del Sur) a grandes fortunas españolas, que se están fugando de Panamá a toda velocidad tras las revelaciones de los “papeles”, es decir, las sociedades opacas controladas por los abogados Mossack-Fonseca.

Según confirman a El Confidencial Digital varios importantes despachos fiscales de Madrid, el escándalo de los “papeles de Panamá” está provocando un traslado masivo de cuentas bancarias de españoles desde el país centroamericano a Estados Unidos. También están recibiendo órdenes, además, de que los cambien desde otros territorios como Suiza y Luxemburgo.

Entradas de dinero en Estados Unidos

Los asesores financieros han descubierto una inmensa oportunidad de negocio porque han dado con diversas fórmulas que, rozando la legalidad vigente, permiten acercar las grandes fortunas a bancos norteamericanos y mantenerlas en el anonimato.

Según datos del sector, cada año vienen entrando en Estados Unidos 1.400 millones de euros de dinero negro, con el objetivo de conseguir privacidad, y en muchos casos la evasión de impuestos en los países de origen.

Necesidad de proteger la riqueza

Los despachos fiscales españoles consultados por ECD reconocen que están trasladando a los grandes patrimonios la necesidad de que los propietarios de fortunas mantengan su privacidad en secreto para evitar posibles secuestros o extorsiones.

Por este motivo, les recomiendan ocultar su riqueza. El paso siguiente es mostrarles la facilidad que existe en estos casos a la hora de evitar impuestos y eludir pagos cruzados.

No obstante, tienen especial cuidado con clientes que proceden de países en los que la corrupción es un realidad muy extendida. Por eso, antes de aceptar a un nuevo cliente elaboran un estudio que acredite la procedencia limpia del dinero.

Al margen de normativas internacionales

Como bien conocen los despachos fiscales, Estados Unidos está últimamente marcando distancias con las normativas internacionales, aprobadas en los últimos años, relacionadas con la divulgación de información.

Barack Obama aprobó en 2010 la ley FATCA, que obliga a las entidades financieras a notificar las cuentas de los ciudadanos norteamericanos que se hallan en el extranjero. Las multas, en el caso de no cumplir la ley, son muy elevadas.

Sin embargo, la OCDE (Organización para la Cooperación y el Desarrollo Económico) sacó adelante posteriormente una normativa bastante más severa para descubrir y castigar a los evasores fiscales. La aplicación de esta nueva legislación comenzó el año pasado, con el acuerdo de los 97 países pertenecientes a este organismo. Pero hubo cuatro excepciones: Nauru, Vanuatu y Bahréin… y Estados Unidos.

La decisión de Washington provoca sospechas entre los expertos fiscales. Llama la atención que Estados Unidos decline de repente acogerse a la normativa de la OCDE, cuando se venía caracterizando por abanderar la lucha contra los paraísos fiscales y la evasión de capitales. La conclusión es que ha dado un giro y va camino de convertirse en todo un paraíso fiscal.

Esta circunstancia está dejando un amplio campo a los despachos de abogados para la evasión fiscal en EE.UU. Un agujero por el que, confirman, es fácil colarse y salir indemne.

Mayor privacidad que en Suiza o las Islas Caimán

La lucha de Estados Unidos contra estas prácticas era tal que las grandes fortunas norteamericanas optaban por refugiar sus capitales en paraísos fiscales como Suiza, Luxemburgo o las Islas Caimán para evadir impuestos.

Ahora, el escenario está cambiando. Los despachos en todo el mundo están recomendando trasladar los fondos a lugares como Nevada, Wyoming y Dakota del Sur, convertidos en los nuevos paraísos fiscales.

El motivo es que la privacidad para ocultar fortunas es ahora mucho mayor en esos estados norteamericanos que en paraísos fiscales hasta ahora de referencia como Suiza, Luxemburgo, las Islas Caimán y el propio Panamá.

Por la incertidumbre económica, hay más consultas para abrir cuentas en el exterior: cuáles son los requisitos

Se debe tener en cuenta la necesidad de concurrir personalmente, la disponibilidad de ese dinero, el asesoramiento necesario en el caso de inversiones, las cargas tributarias o los pagos de comisiones

Algunas entidades permiten hacer aperturas remotas

La inestabilidad económica y política de los últimos años, sumadas a las abruptas devaluaciones y las medidas de control de cambios implementadas desde el fin de semana, provocaron un aumento en las consultas de argentinos que quieren abrir cuentas en el exterior.

Así lo confirmaron a Infobae, distintos asesores financieros. Sin embargo, los que inician el trámite —siempre con dinero declarado y con justificación del origen de los fondos— tienen que tener en cuenta algunos detalles como la necesidad o no de concurrir personalmente, el tiempo que puede demandar luego la disponibilidad de ese dinero, el asesoramiento necesario en el caso de inversiones, las cargas tributarias o los pagos de comisiones, que varían según el tipo de entidad bancaria, de cuenta y, sobretodo, del país.

Una vez que se deposita el dinero en inversiones fuera del país hay que tener en cuenta que el acceso al capital puede no ser inmediato o con la rapidez que el inversor busca

En muchos casos, una vez que se deposita el dinero en inversiones fuera del país hay que tener en cuenta que el acceso al capital puede no ser inmediato o con la rapidez que el inversor busca. Algunos especialistas en inversiones, además, aconsejan que no es siempre la mejor opción para montos menores a los USD 50.000.

«La gente tiene como una fiebre de búsqueda de protección y buen asesoramiento. En los últimos días recibí más de 200 consultas y todos quieren lo mismo, protección del capital en moneda dura. No importa tanto dónde, si acá o afuera. Ya que algunos perfiles quieren tener acceso inmediato al capital y si invertís afuera puede no ser algo tan simple», indicó el analista Alejandro Bianchi, quien esta a punto de lanzar el sitio Asesor de Inversiones.

Los Estados Unidos están entre los destinos más elegidos para abrir cuentas

Los destinos más elegidos por los argentinos suelen ser Uruguay y los Estados Unidos. La principal diferencia entre los dos países es que en el caso de Uruguay se requiere la presencia de persona al momento de abrir la cuenta —en el caso de que se haga directamente y no a través de un agente financiero— y se cobran comisiones para depósitos y transferencias. Mientras que en los Estados Unidos, los costos son menoresy se puede realizar la apertura en forma remota.

«En Uruguay hay comisión por girar o por recibir, por ejemplo, o comisiones porcentuales. Eso en otros países ya no existe. Los mantenimiento de cuenta también son más altos», destacó Mariano Sardans, de la consultora de inversiones FDI. En la última semana el especialista recibió un mayor número de consultas, especialmente de personas que nunca habían tenido cuentas fuera del país.

Desde hace dos años, en el país existe la figura de Asesor Global de Inversiones destinado a brindar asesoramiento a clientes e inversores argentinos en el mercado externo

Desde hace dos años, en el país existe la figura de Asesor Global de Inversiones (AGI) destinado a brindar asesoramiento a clientes e inversores argentinos en el mercado externo. Estos agentes están registrados en la Comisión Nacional de Valores (CNV) que los controla. «Es un asesor local pero también alguien a quien reclamar ante una situación de mala praxis, algo que antes no existía. Un plazofijista por ejemplo que de repente se ve metido en inversiones complejas como bitcoin», aseguró Sardans.

¿A partir de qué cantidad de dinero se puede abrir una cuenta fuera del país? El piso depende del tipo de entidad. Algunos bancos pueden exigir pisos de USD 5.000 o USD 10.000. Pero algunos especialistas sugieren que tener cuentas o inversiones en el exterior se justifica en el caso de sumas mayores a los USD 50.000.

«Por menos de USD 50.000 no conviene invertir en el exterior porque hay alternativas en el mercado local que inclusive han sobrevivido al corralito del 2001 como la caución bursátil«, detalló Bianchi. La caución bursátil es un préstamo de corto plazo (de 7 a 120 días) con una garantía del Mercado de Valores y que se asemeja a un plazo fijo.

Según Bianchi, otra condición a tener en cuenta es que invertir en el exterior tampoco es una alternativa para alguien que quiere disponer inmediatamente de su dinero. Se recomienda más para una inversión de largo plazo, de tres a cinco años como mínimo.

Desde el punto de vista impositivo, las cuentas en el exterior tributan varios impuestos

Desde el punto de vista impositivo, las cuentas en el exterior tributan varios impuestos. «Las cajas de ahorro en dólares radicadas en la Argentina están exentas del impuesto a los bienes personales, mientras que las cuentas en el exterior se encuentran gravadas», explicó el especialista en temas tributarios Iván Sasovsky, titular del estudio Sasovsky y Asociados.

También recordó que para poder abrir una cuenta en el exterior o realizar una transferencia se necesita siempre que esos fondos estén declarados y se justifique cuál es su origen.

Los argentinos buscan preservan ahorros en dólares

«Hoy, Estados Unidos es el único país importante del mundo que no firmó el intercambio de información financiera (CRS) que adoptaron la mayoría de los países del mundo para intercambiar información financiera entre los distintos países. Al no suscribirlo prácticamente se convirtió en un nuevo paraíso fiscal internacional«, advirtió Sasovsky.

Además, indicó que luego del «blanqueo» de 2017, gran parte de las cuentas de argentinos en el exterior fueron declaradas. «Eso hizo que el proceso de transferencia hacia cuentas propias en el exterior sea mucho más fácil«, detalló.

Según los datos del blanqueo, en 2017 los argentinos declararon y regularizaron cuentas en el exterior por USD 25.900 millones e inversiones por USD 55.000 millones también fuera del país.

El desafío financiero para los mexicanos del siglo XXI

Por Gustavo Ibáñez Padilla.

En México el 95% de los trabajadores independientes no dispone de un Plan de ahorro para el retiro, lo que plantea un desafío importante para sus familias. El problema se agrava con el paso de los años, ya que se estima que en 2050 un tercio de la población mexicana será mayor de 60 años.

Según datos estadísticos oficiales, cada día 799 mexicanos cumplen 60 años, lo cual representa al cabo de un año casi 300.000 personas.

Una encuesta privada evidenció que el mexicano promedio muestra cierta desconexión entre sus prioridades de vida y las acciones que toma, ya que coloca al retiro como la cuarta prioridad -después de casa propia, herencia para la siguiente generación y educación de los hijos- pero son muy pocos los que ahorran para su jubilación.

Según datos de la CONDUSEF (Comisión Nacional para la Protección y Defensa de los Usuarios de Servicios Financieros), el 57% de los mexicanos ahorra dinero de manera informal; más de la mitad lo hace atesorando en casa; 32% en tandas y el resto lo guardan con familiares o en cajas de ahorro.

Como podemos ver, estas modalidades de ahorro son riesgosas y poco productivas. Atesorar en el colchón implica riesgos de pérdida o robo y no produce interés. Lo mismo da que sea en la propia casa o con familiares.

Ahorrar en Cajas de Ahorro tiene muy bajo rendimiento y es muy probable que recurramos a dichos fondos en un período corto de tiempo, ya que no hay barreras que dificulten los retiros.

Ahorrar en tandas es una costumbre muy popular en México, que consiste en reunir a un grupo de personas, quienes al participar se comprometen a aportar un monto fijo cada semana, mes o quincena. En cada periodo, el dinero reunido, se sortea entre los participantes. Los ganadores reciben la cantidad total y ya no participan en los sorteos posteriores, aunque mantienen su obligación de continuar aportando. Al final, todos los participantes terminan recibiendo su ahorro. En Argentina, esta modalidad suele conocerse como Círculo de Ahorro; pero usualmente es organizado por una empresa y no en la modalidad informal como ocurre en México.

La ventaja de ahorrar en tandas es que resulta posible alcanzar nuestro objetivo de ahorro antes (si salimos sorteados al principio) que si lo hiciéramos por separado. Esto significa que también son utilizadas como mecanismo de financiamiento.

El riesgo de ahorrar en tandas es que por ser un mecanismo informal, las personas que ya salieron sorteadas pueden dejar de aportar -en perjuicio de los demás- lo cual sucede con mucha frecuencia. Además, existe el riesgo de que el organizador, que reúne los aportes, desaparezca con los fondos.

Es importante destacar que ahorrar en tandas no implica una inversión, por lo cual no genera rendimientos; y además este sistema informal enfoca a las personas en un ahorro de corto plazo generalmente orientado al consumo y no a la inversión.

Esta realidad de la cultura financiera mexicana muestra la importancia y la necesidad de fomentar y difundir los mecanismos específicos de ahorro e inversión de largo plazo, es decir, los Seguros de Vida y las Anualidades.

Es muy accesible a cualquier persona con ingresos diseñar su Plan Personal de Retiro, mediante una póliza de Seguro de Vida con capitalización. También pude recurrirse a las Anualidades (contratos de inversión en una compañía de seguros de vida) para financiar los estudios de los hijos o planificar el retiro. Por supuesto, esto debe realizarse con el asesoramiento de un Consultor Financiero, que optimice el rendimiento de dichos instrumentos financieros.

A fin de lograr los cambios culturales necesarios que permiten crear hábitos financieros saludables, que reemplacen las costumbres perniciosas, es indispensable promover la Educación Financiera de todas las personas y desde la edad más temprana posible. El ahorro y la inversión son demasiado importantes para ser librados al azar y al voluntarismo.

Two great Dave Ramsey myths, debunked Seriously, Dave?

By Michael Markey – Mar 23, 2015.

Personal finance guru Dave Ramsey works in his broadcast studio in Brentwood, Tenn., on March 23, 2006. (AP Photo/Mark Humphrey)

Last month, I wrote about the Seven steps Dave Ramsey followers really need to thrive financially. I was astonished with the amount of interest and debate the piece sparked. To the many who support our voyage, thank you and I’m excited to walk with you down this path, holding America’s Favorite Finance Coach accountable for his investment advice. To the critics who believe anyone disagreeing with the guru means they haven’t read his books, listened to his show, or attended his FPU … you’re wrong, wrong, and right. I have not attended FPU nor do I intend to. I don’t need to smoke a cigarette to know they stink, cost lots of money, and are negative for my long-term health. Financial Peace University is taught by those who’ve mistakenly taken a myth for a truth.

This sort of mix-up is one that Dave is familiar with.

«I have heard it said that if you tell a lie often enough, loudly enough, and long enough, the myth will become a fact. Repetition, volume, and longevity will twist and turn a myth, or a lie, into a commonly accepted way of doing things.»

-David L. Ramsey III “The Total Money Makeover” (TTMM)

Hmm … 12 percent annualized rates of return, 8 percent safe withdrawal rates, no debt EVER, 7 percent mortgage rates used to debunk the tax benefits of mortgage interest, 100 percent stock-based mutual fund portfolios, asset allocation is a dupe, term insurance is better than permanent … I could keep going but I think you get the point. Many of Dave’s truths are actually myths, but they’re said often enough and passionately enough that their validity is accepted without challenge.

Myth No. 1: The Ramsey brand of endorsement benefits clients and advisors.

Let’s turn our attention toward a classic Ramsey-backed idea: the endorsed local provider, or ELP. To be or not to be an ELP, that is the question.

Working with an ELP or an investing advisor (Dave’s fictitious title, not mine) is recommended in Step 4of Dave’s seven-step plan. Please note that an investing advisor is not the same thing as an investment advisor representative (IAR). They get paid to sell you something not give you advice. But that’s not the real issue here. The real issue is I don’t think Dave actually believes in some of the core teachings he spouts with, as he puts it, “extreme confidence.”

It’s important to note up-front that Dave’s entire marketing plan points to the fact that his recommended advisors must be commission-based, rather than fee-based. Instead of going into his reasons, let’s take a look at the facts.

Fact: Investment advisors are prohibited from using endorsement. SEC Rule 206(4)-1(a)(1) of the Investment Advisers Act of 1940 determined testimonials or endorsements are a form of misleading advertising since they only share positive experiences.

Fact: The statement found on Dave’s site, “98 percent of users highly recommend using an ELP” would most likely be in violation of SEC Rule 206(4)-1(a)1.

Fact: The very term Endorsed Local Providers would also most likely violate the above rule. I suppose you could argue he could rename them Dave’s Elite Squadron of Advisors. (Dave, if you’re reading this, feel free to use this term. No royalties needed.)

Fact: If ELPs were IARs they would have to disclose they pay a fee for the clients referred to them by the Ramsey system.

Fact: Working in a fee-based relationship would make it nearly impossible for ELPs to take on the types of clients Dave sends their way.

Fact: Dave states he at some point held the appropriate investment, insurance, or real-estate licensing to give advice in the applicable areas. I could not find a currently registered or previously registered IAR or FA whose full name matched or was from the Tennessee area.

OK, so, if the name is no longer ELP and we remove Dave’s endorsement (he could still use his name in the agency titling, or advertise the firm on his site and his workshops with much success, I’m sure) and we omitted that 98 percent of users highly recommend an ELP, then his team could work as fee-based advisors, right? Not quite. Even if the necessary changes were made to Dave’s marketing approach, a fee-based advisor would very likely starve by working as an ELP.

Let’s look at the math behind all of this. While it was impossible to find the exact referral fee paid to Ramsey for the endorsement, multiple Google searches revealed fees ranging from a few hundred dollars well into the thousands. For the purpose of this column, let’s settle on a referral fee of $100 dollars, which seems reasonable compared to other lead sources.

Now, here’s the math for an American household with an annual income of $48,000 (the average annual wage for U.S. households, as provided by Dave) that is looking to invest 15% of said annual income, per Dave’s Step 4.

Average American household income: $48,000.

Example of 401k Employer Match: 3%

$48,000 x 15% = $7,200

$48,000 x 3% 401k employee contribution (to max out employer match): $1,440

$7,200- $1,440 = $5,760 left to invest with ELP per year, or $480 per month.

In scenario one, let’s consider an ELP who is fee-based at 1 percent AUM. ELPs must have the heart of a teacher, not a salesperson. So we can assume they’d meet with the client a few times prior to making any recommendations. After investing 2–3 hours (roughly 1 hour per appointment) the ELP accepts a check from our client in the amount of $480. For the purposes of our example, let’s assume the initial investment takes place at the beginning of a quarterly billing cycle. Over the cycle, there’s $1,440 invested, but only an average balance of $960. The ELP would be entitled to one quarter’s advisory fees of .25% (1% divided by 4 quarters). In other words, our ELP would make a whopping $2.40 for 3+ hours of work.

But Mike, you’ve forgot these fees add up! Why, yes, they do. One full year later the client’s balance will be $6,087. (I used the conservative, widely-agreed-upon, historical S&P 500 12 percent average rate of return.) If billed at that amount, our ELP would make a meager $15.22 for the first quarter billing. I even rounded up.

First year total fee compensation: $37.48

Second year total fee compensation: $103.11

Total compensation, first two years combined $140.59

I know ELPs are supposed to have the heart of a teacher, but in a fee-based relationship they certainly wouldn’t be compensated as much as one. If the ELP were to meet with the client a few times at the beginning and once a year for the first two years, then our ELP would have at least 5 hours invested with them. If we subtract $100 from the total fees paid to the advisor of $140.59 (remember, this is going to Dave for the referral), then our ELP is left with $40.59 for two years’ worth of work.

Let that sink in for a moment, then we’ll move on to scenario two.

This time, our ELP is commission-based and uses mutual funds with 5.75 percent upfront sales charges. Every month, the ELP will make $27.60. He or she will also have some ongoing compensation from the funds sold and kept. Yet just the commissions will equal $662.40 over the two-year span. Subtract the $100 referral fee and you’re left with $562.40. That’s $521.81 greater than our first scenario.

Here are a few other things to consider. Will the ELP convert every referral? Not likely. Let’s say he or she converts 70 percent of referrals. Most referral services, and presumably this one as well, charge per referral sent, not per referral captured. So, 10 referrals equals seven clients.

Here’s the fee-based total over two years:

7 x $140.59= $984.31 minus $1,000 (10 referrals at $100/ea.) = ($15.69)

Here’s the commission-based total over two years:

7 x $662.40= $4,636.80 minus $1,000 (10 referrals at $100/ea.)= $3,636.80

Our fee-based ELP is in the red after two years. This person has worked for FREE for two years! What if they got two referrals per month rather than 10 referrals over two years? I’m not going to bore you with prorating them, let’s just use the same math as above. Two referrals leads to 16 clients (yes, 70 percent of 24 is 16.8 however you can’t have a partial person; we only count whole people here) which gives us a loss of $150.56.

How many 100-percent altruistic advisors do you expect are out there?

Myth No. 2: Invest Dave’s way, and you can expect a 12 percent annualized rate of return.

I said earlier Dave doesn’t even believe his own math. He defines long-term investing as five years or longer. He then says to pick out a “good” mutual fund. Dave says never finance a car, yet today you can finance a used car for 1–3 percent. (Dave and I agree new cars are highly depreciable and often a poor choice.) If you can make a 12 percent average on your good ole mutual funds, then why wouldn’t you invest the $10,000 car fund and make payments? Oh, because if you play with snakes you will get bitten! But here’s the thing: We’re talking about folks who have completed Steps 1–3 and are midway through Step 4. They’ve got a robust emergency savings now and no debt. Couldn’t they afford to do this? Haven’t they proved they have the discipline to be financially responsible?

Dave clearly doesn’t believe in the 12 percent returns fallacy. Why? Ask this question: What about a mortgage? You don’t ever want a mortgage longer than 15 years, according to the guru. What about the tax deduction CPAs tout? “I can do the math,” Dave says. Why pay $7,000 in mortgage interest (7 percent is his number, not mine) on a $100,000 mortgage to save $2,100 in taxes (he uses 30 percent). Um … I can do math, too. One hundred thousand dollars will make 12 percent. Twelve percent interest on $100,000 is $12,000. Mortgage rates are 4 percent, not 7 percent. And let’s use the more typical federal bracket of 15 percent, since the 30 percent pertains to higher income individuals who are certainly NOT using his advice.

OK, so $12,000 in interest. We’ll assume gains are taxed as capital gains, since I can’t imagine how he’d argue for using IRA dollars to pay off the mortgage. So, here’s what we have:

$12,000 – $4,000 in mortgage interest paid + $600 tax deduction = $8,600 (capital gains tax should not be applicable)

That’s right: If you believe in 12 percent long-term averages, you do not pay off your mortgage early. And you will not be bitten by snakes because you have discipline. You have proven your discipline by accumulating 3–6 months’ worth of expenses in cash savings and by paying off all of your debts, according to the earlier steps in Dave’s plan.

If all of this is true, Dave Ramsey doesn’t believe in 12 percent returns for long-term averaging and neither should anyone else.

The big picture

There are many great advisors out there. Many of these hardworking, honest, sincere, and genuine advisors also happen to be ELPs. ELPs are not bad. Commission-based investing has its place. The collage of contradictions and inaccuracies related to Dave’s “investing advisors” and his “investment” advice are what bother me.

I’m very lucky to be walking this journey with you all. Thank you for your support. Help me hold America’s Favorite Finance Coach accountable to his words by emailing my editor nmorford@alm.com with any thoughts or questions. And, in the words of all of our mothers, “words hurt people; choose them wisely.”

Source: Life Health PRO.

Michael Markey

About the Author

Michael is a co-founder and owner of Legacy Financial Network and its associated companies. His vision has expanded the organization from one location to three, with the hopes to make Legacy a nationwide company. He attained his Bachelor’s degree from Eastern Michigan University while playing baseball for the Eagles. Currently, he attends Northwestern University where he’s completing a post graduate degree in financial planning.

Michael’s accolades include being recognized as the trainer of the year for a previous insurance employer and being a Million Dollar Round Table member in 2010, ’11, ’12, ’13. He earned Court of the Table honors in ’11 and ’12 and Top of the Table honors in ’13. You can hear him locally on 102.9 FM every Thursday at 11 am for his weekly radio show, “Financially Tuned.”

In addition to being an Investment Advisor Representative for LFN Advisors LLC, and an Insurance Agent for Legacy Financial Network, Michael’s main passions are his family and his faith. He shares his faith with his clients and incorporates it into the Legacy four step system. If you’re on the lakeshore, you’re likely to see Mike and his family on their 1966 wooden boat during the summer.

These are the 7 steps Dave Ramsey followers really need

Seriously, Dave?

By Michael Markey – Feb 18, 2015.

Ramsey’s tenets sound pretty good … until you actually look at his math. (AP Photo/Josh Anderson,File)

It’s no secret that many financial professionals don’t agree with much of the advice Dave Ramsey gives. This is because his financial assumptions are often false. Yes, he’s entertaining, but truly helpful … not always.

About a year and a half ago, Ramsey used Twitter to lash out at several financial professionals who had been chastising his investing advice. He tweeted:

These comments strike me to the core. Many financial professionals help more people in the course of their career than Dave Ramsey ever will. So this column is for you, the thousands of financial professionals who strap on your boots (boots sounds tougher than nice leather oxford shoes), and spend their days, nights, sometimes their weekends helping everyday Americans struggling with poor spending and savings habits. Every month, I will dissect a piece of Ramsey’s financial advice and hold him accountable to providing sound financial principals instead of idealistic fallacies. If the pen is actually mightier than the sword, then, Sir Dave, I challenge you to a duel of math and wit.

7 baby steps to getting out of debt

Let’s start at the beginning. On his website, Ramsey lists “7 baby steps to getting out of debt.” These steps are the cornerstone to his popular book Total Money Makeover. Like so much of his advice, they sound good until you dig in and challenge the assumptions.

There are savers and spenders in this world. Ramsonites are inherently spenders. If they were savers they wouldn’t need his seven-step system. Spending is an addictive habit, which leads to less and less contentment as time goes by. Other addiction counseling services have found it takes 12 steps to recovery, not seven, but I digress. The table below outlines Dave’s seven steps, and what I believe they should be:

1. Save $1,000 emergency fund

1. Save $5,000 emergency fund

2. Pay off debt using the Debt Snowball

2. Give

3. Save 3-6 month’s worth of expenses

3. Save 3-6 month’s worth of expenses

4. Invest 15% of gross earnings

4. Equally pay off debt using Debt Snowball and invest until debt is eliminated and investing 15% of gross wages.

5. College funding for children

5. Personal decision (pros/cons)

6. Pay off home early

6. Good idea unless close to retirement and using liquid retirement assets

7. Build wealth and give

7. Give MORE!

Now, let’s go through these step by step to illuminate the strengths and weaknesses.

Step one: Save $1,000 for an emergency fund. Ramsey calls for this $1,000 emergency fund to pay for “… those unexpected events in life that you can’t plan for: the loss of a job, an unexpected pregnancy, a faulty car transmission, and the list goes on and on. It’s not a matter of if these events will happen; it’s simply a matter of when they will happen.”

This is a good first step, considering that you can’t save $1,000 before you’ve saved $10 or $100. However, what does $1,000 really prepare you for? By Ramsey’s definition the loss of a job — but if you’re making $12 per hour, then you’ve managed to save a whopping 2 weeks’ worth of wages (cut it in half for a dual earning household). How far will $1,000 go towards an unexpected pregnancy or a faulty car transmission? Dave, when was the last time you paid attention to the actual costs for these sorts of expenses? I’ve got good insurance, yet our last child was still over $3,000 in out of pocket expenses. (And let’s not forget the fact that giving birth typically translates into time off from work, which isn’t always paid.)

This step starts with a few dollars but needs to continue to at least $5,000. Five thousand dollars can help protect families from unexpected life events. One thousand dollars doesn’t come close.

Step two: Pay down debt using the Debt Snowball. Ramsey’s rational is this: If you target the smallest debts first and ignore the ones with the highest interest rates then you’ll be encouraged by the psychological effect of lowering the total number of open accounts. He goes on to recommend that we re-allocate the funds used to pay off each card to the next smallest debt that you owe, so that over time your payments become larger.

Common sense tells us this is a good idea, just like common sense tells us driving faster to an appointment will get us there more quickly … unless of course you happen to go past a police officer. But ask yourself this: Is paying down debt the same as saving? No. Paying down debt is spending your money in a different way. Spenders have debt because they’re spenders. Spending down debt is not the same as saving. As we pay down debt it relieves stress, but it does NOT teach us how to save. What happens if you follow Mr. Ramsey’s advice and suddenly lose your job? Great, you have $1,000 saved and you’ve made extra payments on your Macy’s credit card — remember, the debt snowfall rule says target lowest balances first which would most likely be retail store cards, not universal credit cards or auto loans — but you have no job and no money. Don’t worry, though; you can go buy a nice new Chaps blazer for your job interview.

Step two should be to give. You might be thinking that giving prior to paying down debt only further prolongs a debt-ridden life. It doesn’t, and here’s why. First, at this point you’ve created a reasonable safety net of $5,000. Second, gifting — or tithing, as some call it — is fundamental to becoming a saver. Giving is voluntary; paying down debt is not. As a voluntary practice, it takes discipline to habitually do this each and every month. If you have the discipline to gift every month then you’ve created a lifestyle change. The discipline of gifting is the same as the discipline of saving. Gifting at step two helps yourself and those around you.

Step three: Save 3–6 months’ worth of expenses. I agree with Dave here. I review too many financial plans where people only have a month or so in cash or cash equivalents, with the rest of their assets invested. I always ask, “What would you do in an emergency?” They usually respond with something like, “We’ll put it on the credit card.” While I understand they have the assets available to liquidate after the fact to pay the card balance back off, it’s still more conservative to have this amount of expenses stashed away in the bank. If you’re like me, you’ll even keep this fund partially in cash.

Step four: Invest 15 percent of household income AFTER debts are paid.

I heartily disagree here. Investing and paying down debt should occur simultaneously because, again, you only learn how to save by SAVING and continuing to save. While I’m not advocating debt is good or leveraging is appropriate, I am suggesting that habits are often lost if not continued. Think about the number of New Year’s resolutions to eat and drink healthier that are broken during the Super Bowl weekend and never adhered to again. Don’t stop saving. Instead, invest and pay down debt.

Continuing with step four, Ramsey says to use commission-based investing and to work with an “investing advisor.” While I don’t want to go into great detail on this now, it’s important to note that there’s no such thing as an investing advisor. I guess if you’re not a licensed advisor or an insurance agent, you can make up any title you want. Notice how “investing advisor” sounds very close to “investment advisor;” in fact, Google “investing advisor” and you’ll only get results for “investment advisor.” Ramsey intentionally uses a similar term, since investment advisors are held to a fiduciary standard, whereas investing advisors (who I can only assume are stockbrokers/financial advisors considering the commission structure) are held to a suitability standard as well as the Ramsey standard (#YesI’mHating).

Ramsey calls his legion of investing advisors ELPs, or endorsed local providers. Wonder why he doesn’t believe in a fee-based model? Consider Rule 206(4)-1(a)(1) of the Investment Advisers Act of 1940. (If you don’t recall the specifics, don’t worry. Next month’s column will use facts and math to prove why ELPs can only work in a commission structure.)

Step five: College funding for children. I’m not going to argue about college funding. That’s a choice for each individual to make, and there are good points for each side. Ramsey thinks parents should pay for college, and that’s fine. I think kids will appreciate college more with every one of their own dollars that goes towards it. Additionally, there are practical considerations at stake. If a parent has three children and they don’t start saving until the parent has reached age 30, then they’ve only got 12 years to recoup/save for these expenses per child (36 years until retirement divided by three). On the other hand, each child probably has 40+ years using the same retirement age. But to each their own on this step. I’ve met some people who take great pride in the fact they were able to help their children through school and their kids graduated with no student loans. I don’t think there’s a right answer here.

Step six: Pay off the mortgage. Eliminate the biggest debt most people have … it makes sense, right? This should help individuals need less income in retirement. Again Ramsey almost got it right but missed a very important point. Retirement is about income, not assets. You must have assets to have income, you say? Wrong. Social Security is not an asset, is it? It’s only income. Think about it this way. Many of the people whom I serve would have a very nice retirement with $2,000,000 in assets — unless $1,950,000 is tied up in their home. If that’s the case, then they’re broke. But good news: They’d still have completed Ramsey’s steps 1-6 (assuming Social Security and $50,000 covers 3–6 months’ worth of expenses).

Here’s an example of when step six doesn’t make sense. Last year I helped a husband and wife, one still working and the other retired, but both taking Social Security. They had previously followed the advice of an advisor who I can’t say for certain was an ELP but his plan certainly stunk of one. He had them refinance their home to a 10-year mortgage so they’d pay less interest and get the house paid off in their lifetimes. In order to cover this larger monthly mortgage payment they had to do two things. The husband had to continue to work and they had to withdraw money from their retirement savings each month. We did some simple forecasting using reasonable rates of return based on a Morningstar report and found that, yes, they would get their house paid for in full by their early 70s. At that time, they’d have a $350k house free and clear and about $100k in retirement savings. In the process, they converted a liquid asset (retirement savings) to pay off an illiquid asset (home equity).

I asked if they ever want to leave their home. They replied no, especially not after working the extra years to pay it off. Yet somewhere between their late 70s and early 80s, they’d have to sell or tap into their equity. They weren’t concerned with leaving the house to the kids mortgage-free. They needed to take care of themselves first. The only thing this plan accomplished was more years of working and a debt-free inheritance for the kids … oh, the good life.

Paying off the mortgage can be a noble thing, but it can be absolutely the wrong thing if you’re in retirement or close to retirement. Tying up most of your assets into the place you love and never want to leave is just as harmful as having too much debt. You may have no debt, but you also have no money.

Step seven: Build wealth and give. I agree with Dave that we should give back. The more we get, the more we should give. Again, I think this should happen much earlier because when you learn how to gift you learn how to save. Gifting should really be step two, as I previously stated. This is especially true when you consider that Ramsey preaches much of his advice is faith-based. How on earth can he suggest to give only once someone has received so much? By the time he suggests you give, you’ve saved tens of thousands of dollars for emergencies, you’ve paid off all your debt, you are investing 15 percent of gross wages, you’ve paid or are paying for your children’s college, and you’ve either paid your house off or are close to it. Only then are you supposed to give. In other words, don’t go without so you can help someone else first. Take care of steps 1–6, then learn the word generosity.

This was just the beginning. Today we debunked several of the 7 baby steps, which are core to Dave Ramsey’s “Total Money Makeover.” While the advice wasn’t entirely bad, there are certainly some glaring deficiencies.

I like math — strike that, I love math — and I don’t particularly care for opinions. Remember, this column is for you. If you notice any particular financial advice from Dave you’d like to refute, please email my editor at nmorford@summitpronets.com. I appreciate your help holding America’s favorite finance coach accountable to good, sound financial advice and not just the entertaining garble that most won’t take the time to validate.

Michael is a co-founder and owner of Legacy Financial Network and its associated companies. His vision has expanded the organization from one location to three, with the hopes to make Legacy a nationwide company. He attained his Bachelor’s degree from Eastern Michigan University while playing baseball for the Eagles. Currently, he attends Northwestern University where he’s completing a post graduate degree in financial planning.

Michael’s accolades include being recognized as the trainer of the year for a previous insurance employer and being a Million Dollar Round Table member in 2010, ’11, ’12, ’13. He earned Court of the Table honors in ’11 and ’12 and Top of the Table honors in ’13. You can hear him locally on 102.9 FM every Thursday at 11 am for his weekly radio show, “Financially Tuned.”

In addition to being an Investment Advisor Representative for LFN Advisors LLC, and an Insurance Agent for Legacy Financial Network, Michael’s main passions are his family and his faith. He shares his faith with his clients and incorporates it into the Legacy four step system. If you’re on the lakeshore, you’re likely to see Mike and his family on their 1966 wooden boat during the summer.

/s3.amazonaws.com/arc-wordpress-client-uploads/infobae-wp/wp-content/uploads/2017/02/15124901/millennial-computadora2.jpg)

/s3.amazonaws.com/arc-wordpress-client-uploads/infobae-wp/wp-content/uploads/2018/06/19153620/Nueva-York-bitlicense.jpg)

/s3.amazonaws.com/arc-wordpress-client-uploads/infobae-wp/wp-content/uploads/2017/07/19145350/Monedas-y-Billetes-peso-pesos-plata-dinero-1920-15.jpg)

7 baby steps to getting out of debt

7 baby steps to getting out of debt